In Nigeria’s fast-evolving fintech sector, Moniepoint has emerged as one of the most transformative players, redefining how millions of small businesses and individuals access financial services.

Founded in 2015 by former Interswitch engineers Tosin Eniolorunda and Felix Ike, the company set out to close a critical market gap: the lack of reliable, affordable, and accessible payment infrastructure for Nigeria’s vast informal economy.

What began as a B2B software provider has evolved into a full-fledged financial services platform, powering over 5.2 billion transactions worth more than $150 billion annually and serving more than 2 million businesses.

Through its innovative agent banking model and proprietary technology, Moniepoint has scaled across Nigeria and is now expanding its footprint into other African markets.

This analysis traces inside Moniepoint’s journey, founding story, early challenges, key milestones, and growth strategies, while comparing its trajectory to competitors like OPay and PalmPay.

It also explores the company’s impact on financial inclusion, the challenges it faces in a highly competitive regulatory environment, and the opportunities that lie ahead in shaping Africa’s digital financial future.

Disclaimer: The data in this episode of StoryLab is based on publicly available funding information as of July 2025 from reliable sources such as Startuplist Africa, TechCabal, TechCrunch, Rest of World, and official press releases.

Summary

- Founded in 2015 by Tosin Eniolorunda and Felix Ike: Two former Interswitch software engineers, they bootstrapped TeamApt with a vision of delivering “financial happiness” to underserved businesses. They initially built payment infrastructure for banks (B2B) before pivoting to an agent-banking model with the Moniepoint platform.

- Rapid growth via agent banking: After a ₦5.5M Series A (2019) and a Central Bank switching license, Moniepoint built a network of hundreds of thousands of POS agents (often called “business managers”) across Nigeria. By 2023, it was processing 5.2 billion transactions (≈$150 billion) and powering payments for ~2.3 million small businesses. Year-on-year growth ran 200–300% during 2018–2022, and it achieved unicorn status in late 2024 with a $110M Series C (led by Google/ADP).

- Key milestones: 2019’s launch of the Moniepoint agent-banking app; 2021 business bank/microfinance license (adding loans/credit); rapid Series B/C fundraises (2022–24) with QED, Novastar, etc.; rebranding to Moniepoint (2023) and HQ move to London for global expansion. It now offers Moniepoint Business Banking and the Monnify payments gateway, plus working-capital loans and accounting tools.

- Competitive position: Moniepoint’s strength is its hybrid model: proprietary core banking + vast offline agent network. It claims over half the Nigerian POS market by transaction volume. This contrasts with rivals: OPay (SoftBank-backed) grew via big consumer rewards and rideshare services, built ~563K agents (~37% share), and ~40M users; PalmPay (TAG/Dangote) scales via a “super-app” plus >1 million on-the-ground merchant agents. All target the informal economy, but Moniepoint focuses on B2B2C (MSMEs) while PalmPay/OPay have larger retail user bases.

- Impact & outlook: Moniepoint’s growth has helped bring digital banking and credit to Nigeria’s micro/small businesses (often cash-dependent). By 2023, it had extended basic banking services into previously “unbanked” communities via its agents. Future growth hinges on new markets (e.g., Kenya via Kopo Kopo and Sumac acquisitions), expanding to individual consumers (personal banking launched 2023), and navigating tighter regulation (e.g., 2024 CBN compliance fines of ₦1B).

Founding Vision and Early Years

In mid-2015, Moniepoint was founded as TeamApt Inc. by Tosin Eniolorunda and Felix Ike. Both founders were veteran software engineers (notably at Interswitch) who saw that Nigerian SMEs and informal businesses lacked reliable digital banking and payment tools.

They deliberately took a B2B route at first, selling APIs and payment platforms to banks (products like MoneyTor, AptPay) while they refined their core technology.

Their mission – as Eniolorunda often puts it – was to “create financial happiness” for underserved populations. In pr,actice this meant designing products with simple, low-friction interfaces and using tech to ensure money moved quickly.

Around 2018–2019, TeamApt spotted a market gap: banks in Nigeria were often unreliable at credit transfers, and millions of small traders were still cash-dependent.

The founders launched a Nigerian agent-banking solution, Moniepoint, in 2019 as their first consumer-facing product. Merchants could buy TeamApt’s POS terminals and agent accounts to receive instant transfers and accept card payments.

This solved real pain for store owners: Moniepoint’s terminals boasted lower decline rates and instant transaction reversals, making them preferred by shoppers.

In short order, Moniepoint became ubiquitous: as one Lagos merchant told Rest of World, customers would insist on paying with the Moniepoint machine because “if you use the other terminal, [shoppers] will say, ‘Please use Moniepoint’.

Read Also: Top 15 Grants for African Startups This Year

Key milestones

- 2015: TeamApt founded (Lagos).

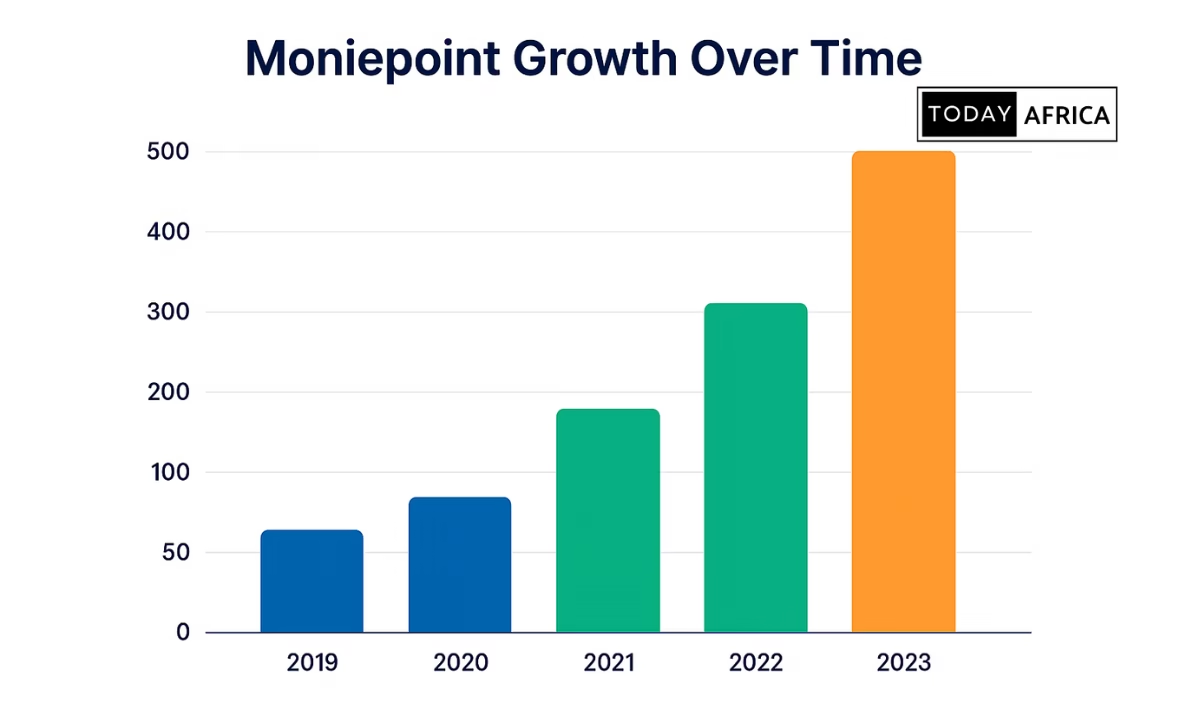

- 2018–2019: Pilot of Moniepoint POS network (agency banking). In March 2019, TeamApt closed a $5.5M Series A (led by Quantum Capital) to scale operations. It also obtained a CBN switching license for payments that year. By late 2019, TeamApt’s Moniepoint app had already processed billions monthly – TechCabal reported ~$4 billion in payments per month in 2021.

- 2020–2021: Rapid growth. TeamApt (still bootstrapped) handled ₦400 billion monthly (~$1.0 billion) by 2021. Annualized transaction volume surpassed $100 billion through Moniepoint and TeamApt’s web-payments gateway Monnify. In 2021, it raised undisclosed Series B funding (led by Novastar). That year, Moniepoint had ~120,000 active agents and served ~18 million unique customers.

- April 2022: Received a microfinance bank license (NDIC), transforming Moniepoint into a full-fledged business bank. It could now collect deposits and extend loans. By year-end 2022, it had issued >$1.4 billion in working-capital loans to businesses (with <0.1% default).

- August 2022: QED Investors led a ~$50M round (pre‑Series C) into TeamApt, marking QED’s first African investment. By then Moniepoint served ~400,000 SMEs in Nigeria, and TeamApt was profitable (over $100M annualized revenue).

- January 2023: TeamApt officially rebranded to Moniepoint Inc., adopting the Moniepoint name globally. (The HQ was moved to London to support global ambitions) This aligned the corporate brand with its well-known POS product.

- July 2023: Moniepoint launched a personal banking app, moving beyond its small-business roots.

- Aug 2023: It moved to deepen its footprint across Africa, it cleared the Kenyan regulator’s approval to acquire Kopo Kopo (a Kenyan payments/lending platform).

- Oct 2024: Announced a $110M Series C, led by Google’s Africa Investment Fund and ADP III. Moniepoint’s valuation crossed $1 billion, making it Nigeria’s newest fintech unicorn. That same year, it was ranked #2 on the Financial Times Africa’s Fastest Growing list.

- 2024–2025: Continued funding and expansion. In Jan 2025, Moniepoint raised undisclosed funding from Visa. (following its Series C). In mid-2025, Moniepoint got CAK approval to buy a 78% stake in Sumac Microfinance Bank in Kenya, providing an on-the-ground banking license for East Africa.

Moniepoint’s funding history

| Year | Funding Round | Amount Raised | Key Investors | Notes |

|---|---|---|---|---|

| 2019 | Series A | $5.5 million | Quantum Capital Partners | To scale banking infrastructure and launch Moniepoint’s agent banking network. |

| 2021 | Series B | Undisclosed (est. $20–25M) | Novastar Ventures, Global Ventures | Enabled Moniepoint’s microfinance bank licensing and merchant loan services. |

| 2022 | Pre-Series C | $50 million | QED Investors (first Africa investment), Novastar, FMO | Supported expansion of SME banking and acquisition of working-capital loan customers. |

| 2024 | Series C | $110 million | Google’s Africa Investment Fund, ADP III | Marked unicorn status (~$1B valuation); funding to fuel African expansion (Kenya, etc.). |

| 2025 | Strategic Investment | Undisclosed (Visa investment) | Visa | Strategic partnership for card issuance, payment rails, and potential remittance products. |

Growth Strategy and Business Model

Moniepoint’s success springs from several interlocking strategies:

1. Agent banking network

The company built a vast network of on-the-ground agents (“business managers”) who recruit merchants and distribute POS devices. By early 2024, this network surpassed 600,000 agents; Techpoint data (Dec 2022) put Moniepoint at ~304,000 agents (~20% share).

Agents earn commissions for each transaction, an attractive income source. Moniepoint studied informal networks (e.g., transport unions, church groups) to identify and recruit reliable local entrepreneurs as agents. This hybrid distribution (digital app + human agent) “built trust” in low-tech markets.

2. Proprietary tech and reliability

Unlike many fintechs relying on third-party core banks, Moniepoint built much of its core payment infrastructure in-house. This allowed it to optimize uptime and offer faster settlements.

Merchants note Moniepoint terminals have lower decline rates and instant reversals, critical in Nigeria’s high-volume retail environment.

During Nigeria’s 2023 cash crisis (new currency rollout), Moniepoint’s network reportedly “came to the rescue” for many businesses struggling to get paid.

3. Regulated financial services

Holding a microfinance bank license allows Moniepoint to take deposits, extend credit, and bundle banking services. Its suite includes business checking accounts, POS terminal services, payment gateway (Monnify), expense management (prepaid cards), bookkeeping tools, and insurance products.

This full-stack offering creates multiple revenue streams: fees from POS transactions and e-payments, interest on loans, interchange on cards, etc.

By 2023, Moniepoint’s strategy of pairing lending with agent onboarding meant many merchants (e.g., market traders) would get small loans and then become paying customers.

Moniepoint claims many of its credit users were previously unbanked: it innovated social-based underwriting (using a trader’s network reputation to score credit) to onboard informal businesses.

4. Customer acquisition tactics

Moniepoint’s front-line agents do much of the marketing, physically enrolling merchants and explaining the product. This grass-roots approach contrasts with OPay’s earlier mass giveaways or PalmPay’s aggressive digital promos.

Agents often provide basic training and support, deepening loyalty. The company also leverages strategic partnerships: for example, it has tied in with Google to digitize merchant records, and collaborates with card schemes (recently issuing millions of branded Verve cards with AfriGo).

Its 2024 partnership with Visa (investment deal) hints at further ecosystem tie-ups (Visa pre-paid cards, international remittance, etc.).

20 Most Funded Startups in Africa Still Active This Year

Competitive Industry: OPay and PalmPay

Nigeria’s fintech scene is crowded. Moniepoint’s main peers are OPay and PalmPay, both of which also target the mass and SME markets but with different models:

OPay

Backed by China’s Opera Group (SoftBank, Sequoia), OPay entered Nigeria with a broad strategy: motorcycle rideshare, food delivery, and a mobile wallet in 2018.

It attracted ~40 million registered users by 2023, largely via subsidies and agent cash-in networks. OPay built ~563,000 PoS agents by end-2022 (37% of Nigeria’s market).

However, many of its early services (bikeshare, foreign remittances) later wound down. Today OPay focuses on payments, transfers, and loans, but faces tighter regulation and scaled back ambitions.

By contrast, Moniepoint never chased consumer glamor projects – it stuck to payments/infrastructure – and claims higher reliability.

In June 2023, OPay held ~37% of POS agents vs Moniepoint’s ~20%, but Moniepoint’s revenue/share is boosted by its microfinance bank license and suite of B2B products (lending, cards).

PalmPay

Launched in 2019 by Tech giants (Transsion Holdings and NetEase), with strategic backing from MediaTek. PalmPay is a “neobank” aiming at underserved consumers and has 35 million registered users and up to 15 million daily transactions as of 2025.

Like Moniepoint, PalmPay blends digital apps with physical agents: it claims over 1 million merchants/agents on the ground. PalmPay’s super-app offers zero-fee transfers, credit, savings, and insurance.

Its growth has been explosive (2020–2023 CAGR ~584%) because of aggressive agent recruitment and deep promos. Importantly, TechCrunch notes PalmPay’s model “builds on the realities of Africa’s informal economy” by onboarding shop merchants as entry points.

This hybrid approach mirrors Moniepoint’s own strategy, though PalmPay’s customer base skews C2C and retail. Moniepoint, in comparison, sticks closer to business banking, targeting that same informal economy by giving traders not just payments but working-capital loans and tools.

In summary, Moniepoint competes by focusing tightly on SME banking and payment infrastructure rather than consumer lifestyles. Its key edge is owning multiple regulatory licenses (microfinance, switching) and an agent-based rollout that some analysts say reaches half of offline merchants.

Financial Performance and Scale

Though Moniepoint is privately held, public data illustrate its scale:

Transaction volume

2021 saw ~$4 billion monthly; by 2022, annualized volume topped $170 billion. In 2023, Rest of World reported ~5.2 billion transactions worth >$150 billion. (Nairametrics similarly noted Moniepoint jumped from ₦400 billion/month in 2021 to ₦8 trillion by mid-2023, reflecting the cash-crunch-driven surge.) This puts Moniepoint in league with Flutterwave/OPay in payment throughput.

Customers & merchants

By end-2022, Moniepoint counted ~1.3 million merchant clients; by Jan 2024, about 2.3 million businesses were using its POS terminals. It has over one million business clients (SMEs) across Nigeria and “thousands” of banking agents. Unlike consumer fintechs, Moniepoint doesn’t tout “users” in the tens of millions, but its aggregate merchant base likely reaches tens of millions of end-customers (through cards/transfers).

Revenue and profitability

In 2021, TeamApt was already generating ~$100 million annualized revenue, growing ~300% annually (2018–21). Nairametrics confirms this steep growth and notes Moniepoint was profitable before its big Series C.

(By contrast, OPay’s losses were widely reported, and PalmPay only turned a profit recently despite massive scale.) Moniepoint’s revenues come from transaction fees, interchange, and interest margins. Specific 2024 figures aren’t public, but the company’s unicorn valuation implies strong financials.

See Also: These 3 Entrepreneurs are Revolutionizing Agriculture in Tanzania

Impact on Financial Inclusion

Moniepoint’s model has significant implications for inclusion:

1. Serving the unbanked

By placing bank-like services in neighborhoods, Moniepoint brings formal finance to people who might never visit a branch. For many first-time customers, Moniepoint provides the first “real” bank account.

Indeed, Nairametrics reports that a quarter of PalmPay’s users say it was their first financial account – Moniepoint’s positioning is similar for merchants. The business managers often act as human “branch-less bankers,” guiding micro-entrepreneurs through digital accounts and loans.

2. Enabling small enterprises

The working-capital loans (often $100–$400) that Moniepoint extended to market traders and petty traders have become a critical lifeline. The founders cite examples of open-market merchants borrowing via Moniepoint who previously couldn’t get bank credit.

This credit boost helps businesses grow inventory, increasing incomes. By 2023, Moniepoint disbursed >$1 billion in such loans with negligible default (claimed <0.1%), suggesting many microbusinesses can be banked once offered the right products.

3. Agent empowerment

The commissioned agents themselves enjoy entrepreneurship. A Rest of World profile shows agents earning unlimited commissions (often more than a salary) by signing up merchants. This creates jobs in impoverished areas (some distributors report building $5–$50 of income on $5.44 signup fees plus ongoing fees).

4. Digital payments growth

By early 2024, Moniepoint’s terminals reportedly accounted for 50% of all POS transaction value in Nigeria. That’s a huge step for cashless commerce. Its ubiquity means more businesses accept cards and transfers, moving communities away from cash. The company itself highlights its role in the April 2023 currency exchange crisis, during which its network kept many SMEs operational while cash dried up.

Moniepoint’s accolades reflect this inclusion: it won the Central Bank’s Inclusive Payment Initiative Award and (with other Nigerian firms) featured on Fast Company/FT lists of Africa’s top fintech innovators.

Challenges and Regulatory Environment

Despite success, Moniepoint faces hurdles:

Regulatory scrutiny

In 2023–24 the Central Bank of Nigeria (CBN) began tightening oversight of fintechs. Moniepoint (and OPay) were each fined ₦1 billion in 2024 for various compliance lapses. The root issue: both operate under microfinance bank licenses (intended for small-scale lending) while serving millions.

Regulators worry current licenses may not fully protect consumers at scale. Moniepoint must upgrade its KYC/AML systems (the CBN even temporarily banned new sign-ups for some fintechs over KYC in 2024).

Market competition and saturation

The Nigerian fintech market is extremely competitive. Large players like OPay are aggressively defending market share (sometimes via heavy promotions), and new entrants (like traditional banks’ own agent networks) also encroach. Moniepoint needs to maintain its tech edge and agent relations; reports suggest it has an enviable position in offline payments, but must innovate to stay ahead.

Macroeconomic pressure

Nigeria’s volatile currency and inflation can impact Moniepoint’s loan portfolio and fees. For example, interest rates can affect borrowing costs for its SME customers. However, Moniepoint’s core fees (like a % of transaction value) scale automatically with inflation. Its success during the cash crisis showed resilience, but prolonged economic stress could temper growth.

Operational scale

Managing over 600k agents and millions of transactions requires huge operational support. Downtime can rapidly alienate merchants (who have alternatives). Moniepoint claims <10% daily failure rates and 60% reduced downtime, but it must continually invest in servers and risk controls. Any significant outages could drive merchants back to incumbents or competitors.

Future Opportunities

Continental expansion

The Kenya acquisitions (Kopo Kopo, Sumac) will give it a beachhead in East Africa. Kenya’s mature mobile-money market (Safaricom’s M-Pesa) offers synergy for Moniepoint’s SME tools. Success in Kenya could presage moves into other Anglophone markets like Uganda or Rwanda. Moniepoint also hints at targeting any emerging market with a strong informal sector.

Product extension

Having conquered SME banking, Moniepoint is now dipping into consumer finance. Its July 2023 “Moniepoint Personal Bank” app offers everyday Nigerians digital savings accounts, transfers, and microloans. If it can cross-sell to its existing merchant base (employees or families) it could rapidly scale that segment.

Partnerships and innovation

Backers like Google and Visa suggest future fintech products (e.g. remittances, cross-border trade financing). Moniepoint’s success with social-credit scoring might evolve into sophisticated credit scores/analytics for MSMEs. It could also leverage data (e.g. transaction records) to partner with big retailers or e-commerce platforms.

Financial inclusion impact

There remains huge unbanked potential: Nigeria’s adult banking rate is still around 65%. Moniepoint’s agent model could be replicated in smaller towns. Moreover, its focus on micro-lending provides a template for “banking the unbanked” across Africa. Continued regulatory support (e.g. tiered licenses) will be crucial, but Moniepoint’s sustainable growth could influence policy to favor fintech-driven inclusion.

Read Also: From Idea to IPO: African Startups Making Global Headlines

Why Moniepoint is Growing – Lessons for Startups

Moniepoint’s rise to the top of Nigeria’s fintech ecosystem didn’t happen by chance. It’s the result of bold choices, disciplined strategy, and some missteps that became critical learning points.

Here’s why Moniepoint is succeeding and what others can learn from their wins and mistakes:

1. Laser focus on a niche before diversifying

When Moniepoint (then TeamApt) pivoted in 2019 to agent banking, it zeroed in on small merchants in Nigeria’s informal economy. These were businesses frustrated by failed POS transactions and slow settlements from traditional banks.

Instead of spreading itself thin, Moniepoint focused on this one underserved group. By 2023, it had over 2.3 million small businesses using its services and processed 5.2 billion transactions worth over $150 billion annually (Rest of World, 2023).

2. Invest in proprietary, reliable technology

Unlike many competitors that relied on third-party core banking systems, Moniepoint built its payment switching and settlement infrastructure in-house. This gave it control over reliability and speed.

For example, during Nigeria’s 2023 cash crunch, Moniepoint’s terminals became the preferred option because they offered lower failure rates and instant reversals, keeping businesses operational when other systems failed.

Own the parts of your tech stack that directly impact customer trust. Reliability becomes your strongest moat in high-stakes industries.

3. Leverage a human‑centered distribution model

Moniepoint didn’t rely solely on apps or digital campaigns to reach customers. Instead, it deployed a vast network of over 600,000 “business managers” (agents) who went into markets, shops, and rural communities to onboard merchants and provide face-to-face support.

This was critical in building trust in cash-first environments where people are wary of digital-only solutions. In emerging markets, combine technology with human touchpoints. Empower local “champions” to help onboard and educate customers.

4. Secure the right regulatory licenses early

By obtaining a switching license in 2019 and later a microfinance bank license in 2021, Moniepoint expanded its services beyond payments to include lending, deposits, and issuing cards. This gave it a strategic advantage over rivals still operating under restrictive licenses.

Plan your product roadmap around regulatory milestones. Early compliance and licensing can open up new revenue streams and deepen customer trust.

5. Maintain disciplined unit economics and sustainable growth

Unlike rivals such as OPay, which spent heavily on subsidies to gain users, Moniepoint kept a close eye on profitability. By 2022, it was processing ₦8 trillion monthly transactions and had already become profitable with over $100 million in annualized revenue (TechCabal, 2022).

Growth is important, but sustainable growth with healthy unit economics gives you resilience in market downturns and builds investor confidence.

6. Build multiple revenue streams around your core

After establishing its payments infrastructure, Moniepoint expanded into working-capital loans, prepaid cards, and expense management tools. By 2022, it had issued over $1.4 billion in loans to small businesses, helping them grow while earning interest income.

Once you’ve earned your customers’ trust, introduce adjacent services that increase their lifetime value and make your ecosystem harder to leave.

7. Learn from compliance missteps and iterate quickly

In 2024, Moniepoint was fined ₦1 billion by the Central Bank of Nigeria (CBN) for lapses in its KYC/AML processes as it scaled. While the fine was a setback, it prompted Moniepoint to overhaul its compliance systems and strengthen relationships with regulators.

In highly regulated industries, compliance isn’t optional. Invest early in strong controls, and if mistakes happen, fix them quickly and transparently.

8. Cultivate strategic partnerships and choose wisely

Partnerships with Google (Series C investor) and Visa (2025 investment) brought not just capital but access to cutting-edge technology and global networks.

These alliances are helping Moniepoint prepare for pan-African expansion, starting with Kenya through acquisitions like Kopo Kopo and Sumac Microfinance Bank.

Don’t just seek investors—seek partners who bring expertise, market access, and technology that can accelerate your roadmap.

9. Stay focused on your Mission

While some competitors diversified too quickly into ride-hailing, food delivery, or other “super app” services, Moniepoint stayed focused on SME banking and payments until it built a dominant position.

Only in July 2023 did it launch its personal banking app, and even that was tightly aligned with its core mission of enabling financial inclusion.

Avoid distractions. Stay focused on your mission until you achieve clear dominance, then expand carefully.

Key takeaways for startups (Inside Moniepoint’s journey:)

- Start small, build deep: Focus on solving one core problem for one audience (like Moniepoint did for small merchants).

- Own critical infrastructure: Build your tech stack where reliability and speed are essential.

- Blend human networks with technology: Especially in trust-deficient markets.

- Treat compliance as a growth strategy: The right licenses can unlock new opportunities.

- Grow sustainably, not recklessly: Profitability attracts patient investors.

- Layer products strategically: Start with one offering, then expand into adjacent services.

- Choose investors who can open doors: Capital alone isn’t enough.

- Focus before diversifying: Don’t dilute your team and resources chasing trends.

Moniepoint’s journey shows that disciplined focus, strategic innovation, and strong human networks can create an enduring competitive edge—even in one of the toughest fintech markets in the world.

Moniepoint has executed a carefully calibrated growth strategy. From humble beginnings as a B2B startup, it built one of Africa’s most robust fintech platforms. Strategically, Moniepoint aims to be more than a payments company; it’s shaping up as a digital bank for Africa’s informal economy.

If it navigates regulation and outpaces rivals, it stands poised to remain a fintech leader and inclusion driver across Nigeria and beyond.

Sources: Reputable news and industry sources, including TechCabal, Techpoint Africa, TechCrunch, Rest of World, and African fintech analysis.

Leave a comment and follow us on social media for more tips:

- Facebook: Today Africa

- Instagram: Today Africa

- Twitter: Today Africa

- LinkedIn: Today Africa

- YouTube: Today Africa Studio

2 Comments

Your writing is not only informative but also incredibly inspiring. Thank you for being such a positive influence!

Thank you for finding value in the article.

Comments are closed.