Across Africa, millions of households remain excluded from both reliable energy access and formal financial systems.

This double exclusion has historically limited productivity, slowed educational progress, and perpetuated cycles of poverty. In response, a new generation of enterprises has emerged to bridge these gaps by leveraging technology, mobile money, and innovative financing models.

Among them, M-KOPA stands out as one of the most influential.

The company’s vision was simple yet transformative: combine mobile money with asset financing to allow customers who could not afford large upfront costs to instead pay in manageable daily instalments.

Over the past decade, M-KOPA has expanded into Uganda, Nigeria, and beyond, raised significant investment from global impact funds and commercial partners, and crossed the milestone of millions of customers served.

This is inside M-KOPA’s journey, analyzing its founding story, funding history, growth strategies, competition, societal impact, and challenges.

Disclaimer: The data in this episode of StoryLab is based on publicly available information as of September 2025 from reliable sources such as founder interviews, news reports, M-KOPA press releases, Techcrunch, Africa Global Funds, and African Business.

M-KOPA’s Founding Story

M-KOPA was founded in 2010–2011 by Jesse Moore, Nick Hughes (formerly of Vodafone’s M-Pesa team) and Chad Larson to tackle energy poverty among Africa’s poorest households.

Moore and Hughes have noted that their inspiration came directly from M-Pesa: “I was involved with M-Pesa … when we realised [mobile money] could change things, we quit our jobs and started M-Kopa five years ago”.

M-KOPA launched commercially in Kenya in late 2012, deploying a basic solar home kit (panel, lights, radio and a GSM-enabled pay-as-you-go meter) that sold for a small deposit plus daily micro-payments.

The initial problem was stark: over half a billion Africans lack reliable electricity, relying on expensive kerosene lamps. M-KOPA’s founders saw that by bundling solar power with M-Pesa’s micro-payment technology, they could bridge that gap.

As Moore later explained, by using mobile money “we could provide off-grid power using a [similar] model” to M-Pesa’s payments rails.

Pilot phase

M-KOPA first targeted rural Kenya. Customers paid roughly a $35 down payment and then about $0.50 per day via M-Pesa. After a year’s payments they owned the system outright.

This pay-as-you-go (PAYG) model let poor families replace kerosene with clean solar lighting at an affordable, daily rate. Early growth was steady: by 2015 M-Kopa reported powering 150,000 homes in Kenya, Uganda and Tanzania.

The company built a field sales network to reach customers: within a few years, it had 1,500 local agents and 100 service centers across East Africa.

(For example, when expansion into rural Tanzania proved challenging, M-KOPA found that local banks lacked the needed skills, and instead partnered with Vodacom’s village franchises – training Vodacom agents to demo and sell its kits.)

M-KOPA also secured technology partnerships early on: Safaricom/M-Pesa in Kenya (and MTN/Airtel wallets in Uganda) handled payments, while hardware partners provided reliable solar components.

From the start, M-Kopa planned beyond a single product. After 1–2 years of finishing a solar plan, many customers became eligible for financing other assets.

By the late 2010s, M-KOPA evolved into an asset-financing platform.

It began offering paygo terms on smartphones, LED TVs, refrigerators, clean cookstoves, electric motorcycles and more. (Notably, it partnered with Samsung in Nigeria to “enable access to smartphones” in 2021.)

Jesse Moore described the company as “a mix of a micro-finance, technology, and energy company wrapped up in one” – a blend of sectors that allowed M-KOPA to sell both productive goods and financial services.

By early 2016, Moore noted M-KOPA had sold about 400,000 solar systems across Kenya, Tanzania and Uganda.

Successive product innovations (higher-wattage kits, solar-powered TVs, multi-light systems) and new sales schemes (for example, trade-in programs for older phones) helped retain customers and reduce service costs.

Key milestones

M-KOPA’s early story includes:

- reaching 400,000 connected homes by 2016

- hitting 500,000 by early 2018; and expanding from East Africa into West Africa by 2021

- M-KOPA reported a franchise presence in Ghana by 2016, and launched in Nigeria in mid-2021.

- In late 2023, it announced a pilot in South Africa. (As of 2024, it operates in five countries: Kenya, Uganda, Tanzania (initially), Ghana, Nigeria and South Africa.)

Funding History and Investors

M-KOPA’s capital journey has been marked by a series of large growth rounds, reflecting investor confidence in its social-finance model. The timeline below highlights major fundraising events:

| Year | Round / Type | Amount (USD) | Investors / Purpose |

|---|---|---|---|

| Dec 2013 | Series C (Equity+Debt) | $20.0 million | Led by Commercial Bank of Africa (working capital debt), to scale distribution in East Africa. |

| Feb 2015 | Series D (Equity+Debt) | $12.45 million | Led by LGT Venture Philanthropy (with Lundin Foundation, Treehouse, Blue Haven). Funds to expand products and East Africa base. |

| Dec 2015 | Series E (Equity) | $19.0 million | Led by Generation Investment Mgmt (Richard Branson, Steve Case, existing shareholders). To reach 1 million homes. |

| Feb 2018 | Debt financing | $10.0 million | FinDev Canada and CDC Group. To grow distribution and subsidize loans. |

| Mar 2022 | Series F (Equity) | $75.0 million | Led by Generation / Broadscale, with CDC Group, Lightrock, LGT, Blue Haven, Latitude. To expand beyond solar and into new markets. |

| May 2023 | Debt + Equity | $200.0 million (debt) + $55.0 million (equity) | $200M sustainability-linked debt led by Standard Bank Group (plus IFC, FMO, BIIF, etc.), $55M equity led by Sumitomo Corp. ($36.5M) and supported by Blue Haven, Lightrock, Broadscale, Latitude. To fund smartphone services, new markets and product diversification. |

These investments came from a mix of impact and commercial backers. Early support came from pioneer investors: Swiss impact fund LGT backed M-KOPA in 2011 and led a $12.45M round in 2015.

The Generation Investment Management team (co-founded by Al Gore) and even Virgin’s Richard Branson joined in, underscoring the company’s scalable potential. By 2022 M-KOPA had raised about $100M in equity ,and was ready to scale into multiple new countries and products.

Each funding tranche had a clear use. Funds generally fueled expansion of distribution networks, hiring of agents, and new product development.

For example, the 2015 LGT-led round explicitly aimed “to expand the company’s product range, grow its operating base in East Africa and license its technology to other markets”.

The CDC/FinDev debt in 2018 was earmarked for network growth (supporting more sales agents) and bridging finance. The big Series F in 2022 ($75M) underwrote M-KOPA’s launch of smartphones and new financial services (loans, insurance) as it prepared for West African markets.

In 2023, the combined $255M debt+equity blitz (Standard Bank-led debt and Sumitomo-led equity) was largely aimed at scaling the smartphone channel and extending the platform’s offerings continent-wide

Notably, debt financing became a large part of the mix by 2023: Standard Bank organized over $200M in sustainability-linked debt, while the equity piece attracted strategic global players.

Across these rounds, investors such as CDC Group, FMO, IFC, British International Investment (CDC’s successor), LGT, Generation, Blue Haven Initiative, and regional banks signalled that M-KOPA’s social impact model could also deliver growth.

As M-KOPA’s CFO noted in 2023, these funds were enabling “the business [to] grow its smartphone services, expand its model to new markets and extend its financed product set”.

Read Also: Inside LifeBank’s Journey: Building the “Amazon for Blood” in Africa

Strategies Fueling Growth

Leveraging mobile money and micropayments

From day one, M-KOPA was built on mobile payments, especially Kenya’s Safaricom/M-Pesa. Customers pay daily or weekly via their phones, eliminating the need for cash.

“For about $200, paid in daily instalments of 50 cents, M-KOPA customers can replace dirty kerosene with clean solar…by making payments digitally from their M-Pesa accounts”.

This alignment with existing mobile-money behavior (over 330 million mobile-money accounts now active in SSA) let M-KOPA reach the unbanked. There are no traditional bank branches involved — even collateral is the product itself.

The integration of a GSM SIM in the solar kit enables remote on/off control and real-time payment tracking, a technology foundation that M-KOPA patentably calls M-KOPAnet.

Small, affordable payments (PAYG Model)

Instead of large up-front costs, M-Kopa asks for token deposits and low daily fees. This “lipa polepole” (pay slowly) approach matches the cash-flow of daily-wage earners.

As Moore put it in 2015, “we are proving solar off-grid will be transformative for customers, good for the planet, and profitable for investors”.

In practice, the average financing rate is kept relatively low (about 3.1% monthly interest on financed goods) to remain competitive with informal credit, while still covering costs.

This affordability has driven uptake: a 2024 customer survey found 92% of clients reported that M-KOPA’s financing made technology more affordable, and 80% said their quality of life improved thanks to the products.

Strategic partnerships (telcos, manufacturers, microfinance)

M-KOPA teamed up with key ecosystem players at every step. In each country, it partners with the dominant mobile-money provider (e.g. Safaricom in Kenya, MTN/Airtel in Uganda, Airtel in Nigeria) to ensure seamless payments.

It also partners with electronics manufacturers: for example, Samsung and Airtel helped launch a phone-financing program in Lagos, Nigeria.

M-KOPA’s channel partners include local distributors, retailers and microfinance networks. In Tanzania, for instance, M-Kopa trained and leveraged Vodacom rural franchisees as sales outlets.

By linking to these established networks, M-KOPA dramatically lowered distribution costs and built trust with off-grid consumers.

Expansion into smartphones and other assets

M-KOPA deliberately broadened its scope beyond solar. By about 2019, it launched smartphone financing (starting in Kenya), recognizing that a low-cost phone is another essential tool for unbanked households.

This move has paid off: by 2024, roughly 4 million M-KOPA customers owned smartphones purchased through its financing plans. The smartphones themselves became a gateway to digital inclusion: internet access, mobile banking, and other apps.

Similarly, M-KOPA extended its asset list to include TVs, refrigerators, and even electric motorcycles. Each product follows the same daily-payment logic.

This asset diversification not only met pent-up demand for modern appliances, but it also helped smooth revenue: if solar sales slowed, profits from the booming phone channel could compensate.

See Also: Inside Zipline’s Journey: Redefining Medical Drone Delivery Across Africa

Data-driven lending and credit building

Every micro-payment a customer makes is logged, building a proprietary credit history. M-KOPA uses this rich transaction data and AI analytics to underwrite new loans and cross-sell services.

Early on, this created thousands of new credit records: by 2016, M-KOPA had generated 75,000 positive credit reports at Kenya’s credit bureau. Today, M-KOPA’s analytics (built on its history of daily payments) allow it to offer cash loans and insurance with confidence.

The company emphasizes that its IoT-enabled finance platform “embeds credit into the product through a smart digital connection, giving customers ownership instantly”.

In effect, every M-KOPA customer becomes “bankable” without ever needing a bank account or conventional collateral.

Customer-friendly servicing

M-KOPA invested heavily in local agents and customer support. It recruited and trained thousands of youth as sales agents and technicians in Kenya and Uganda. (By 2018, over 2,000 agents were working in the field, rising to over 14,000 paid agents by 2024.)

These agents not only sell products, but also provide on-site customer education, maintenance and technical support – a “trusted touchpoint” that is vital for rural markets.

By aligning agent incentives (commissions, promotions) with repayment goals, M-KOPA scaled its sales force quickly while maintaining some control over the customer experience.

Together, these strategies enabled exponential growth. A 2023 analysis noted M-KOPA’s model “combines digital micropayments with IoT” to finance assets that become collateral.

The result is a continuous cycle: affordable daily payments → asset access → positive credit history → eligibility for more products.

CEO Jesse Moore captured this dual energy/fintech strategy: “We provide smartphones embedded with financial services that fit the cash flow of daily-income individuals”.

M-KOPA positioned itself not just as a solar company but as a platform for inclusive financial services.

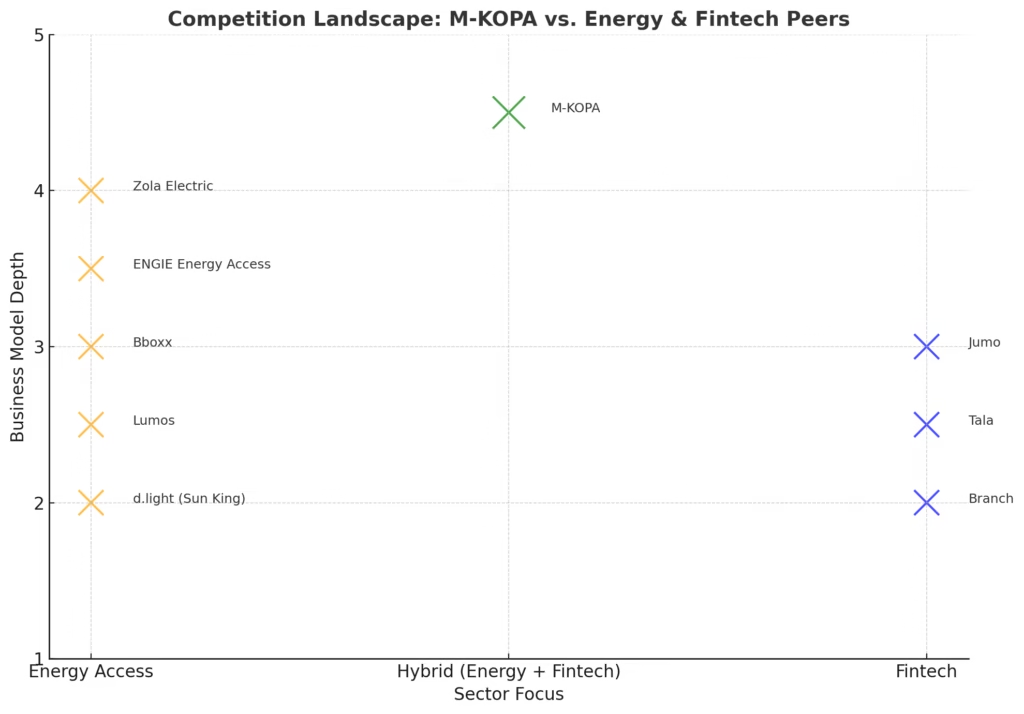

Competition in Energy and Fintech

M-Kopa operates at the intersection of off-grid energy and consumer credit, and thus faces competitors on both fronts.

In the solar/energy access space, its peers include d.light (now Sun King), BBOXX, Zola Electric (formerly Off Grid Electric), ENGIE Energy Access (Lumos), and SunCulture, among others.

These “pay-go” solar startups have attracted the lion’s share of funding: for instance, a 2022 TechCrunch analysis listed the seven most-funded solar PAYG firms as Sun King, Zola, M-Kopa, BBOXX, d.light, Engie, and Lumos.

All these companies offer similar asset-financing for off-grid homes, and compete to reach the same rural customers in Kenya, Uganda, Nigeria, Ghana etc.

In the digital lending/fintech arena, M-KOPA’s competitors include mobile money lenders and digital-credit apps like Branch, Tala, and Jumo. These firms offer micro-loans and pay-as-you-go financing for phones or appliances, targeting the same underbanked segment.

However, most pure-play lenders do not bundle energy products. M-Kopa’s unique edge is its hybrid model: it can start a customer relationship with a solar kit, then upsell a phone, and later offer cash loans or insurance.

As Jesse Moore put it, M-KOPA “does not fit a conventional box – we are a mix of microfinance, technology and energy”. This cross-sector approach differentiates it from rivals that focus solely on one product class.

Nonetheless, competition (and copycats) has been pressure. Alternative models have sprung up, such as PEG Africa (which licenses M-KOPA’s technology) and local solar ventures.

Infrastructure gaps and affordability constraints also limit how far each company can grow. As one report warns, many early-stage off-grid firms struggle to raise capital, and often become “overleveraged” without subsidies.

Even M-KOPA has had to continually innovate to stay ahead: for example, when funding slowed for small players, it leaned on consumer-friendly features (zero late fees, flexible terms) to retain customers.

TL;DR

| Company | Sector | Core Offering | Countries of Operation* | Unique Features / Strengths | How M-KOPA Differentiates Itself |

|---|---|---|---|---|---|

| d.light (Sun King) | Energy | PAYG solar kits, lanterns, home systems | Kenya, Uganda, Nigeria, Tanzania, India | One of the largest PAYG solar companies; deep distribution; affordable entry-level kits | M-KOPA expanded beyond energy into asset financing (phones, TVs, insurance, credit). |

| Bboxx | Energy | Solar home systems, clean cooking, mini-grids | Rwanda, Kenya, DRC, Nigeria, Togo, others | Partnerships with governments (e.g., Rwanda); integrated smart meter tech | M-KOPA leverages mobile money + fintech services; stronger smartphone financing portfolio. |

| Zola Electric | Energy | Solar + battery storage (residential & commercial) | Tanzania, Côte d’Ivoire, Nigeria, Ghana | Hybrid on/off-grid solutions, higher-capacity systems | M-KOPA focuses on low-income households with micro-payments and credit services. |

| Lumos | Energy | PAYG solar systems with telecom partnerships | Nigeria, Côte d’Ivoire | Bundled solar with MTN airtime; telecom-based distribution | M-KOPA diversified financing into digital assets, creating broader fintech ecosystem. |

| ENGIE Energy Access | Energy | Solar PAYG (Fenix Intl.) + mini-grids | Uganda, Zambia, Benin, others | Backed by ENGIE Group; hybrid mini-grid + PAYG solutions | M-KOPA more agile in fintech innovation (credit scoring, smartphone financing). |

| Branch | Fintech | Mobile-based microloans | Kenya, Nigeria, Tanzania, India | Strong data analytics for credit scoring; purely digital lending | M-KOPA combines asset-backed lending (solar/phones) with credit history building. |

| Tala | Fintech | Instant microloans via mobile app | Kenya, Tanzania, Philippines, Mexico | Quick disbursement; strong mobile-first approach | M-KOPA ties lending to productive/essential assets (energy, smartphones), reducing default risk. |

| Jumo | Fintech | Digital financial services platform for banks | South Africa, Kenya, Ghana, Uganda | Provides infrastructure for banks/telecoms to deliver loans | M-KOPA directly interfaces with end-customers through PAYG devices + fintech platform. |

Read Also: Inside Andela’s Journey: How Six People Reimagined Africa’s Tech Future

Impact on Society

1. Expanding energy access

M-KOPA has transformed energy access across Africa by providing affordable solar home systems to households that were previously reliant on kerosene lamps, candles, and diesel generators.

For millions of customers, this shift has meant longer hours of light in the evening, safer homes free from the risks of fire, and healthier living conditions without indoor air pollution.

In rural areas especially, reliable electricity has enabled families to power basic appliances such as radios, televisions, and even small businesses, directly improving productivity and quality of life.

2. Advancing financial inclusion

One of M-KOPA’s most significant contributions has been in financial inclusion. Through its pay-as-you-go (PAYG) model, customers who were previously excluded from the formal banking system are now able to make daily micro-payments via mobile money platforms like M-Pesa.

This system not only makes essential products affordable but also allows customers to establish a repayment track record. Over time, this data forms a credit history, giving them access to loans, insurance, and additional financial services.

By bringing the underbanked into the financial system, M-KOPA is helping to break cycles of poverty and expand economic participation.

3. Driving digital access

Beyond energy, M-KOPA has played a vital role in bridging Africa’s digital divide. Through smartphone financing schemes, customers who could not afford to pay upfront for devices can now own internet-enabled phones.

This access opens doors to mobile banking, e-learning, e-commerce, and communication platforms, allowing individuals and small businesses to thrive in an increasingly digital economy.

In markets such as Kenya, Nigeria, and Uganda, M-KOPA’s smartphone program has been a gateway for millions of people to connect to the internet for the first time.

4. Job creation and skills development

M-KOPA’s impact extends to employment and skills development. The company has built an extensive network of local sales agents, technicians, and customer support staff.

These roles not only provide a steady income but also equip workers with valuable training in sales, financial literacy, and technical support. Many agents gain entrepreneurial experience that they later use to start or scale their own businesses.

By investing in people as much as in products, M-KOPA contributes to both economic empowerment and community resilience.

5. Environmental impact

The shift from kerosene and diesel to solar energy has delivered measurable environmental benefits.

Kerosene lamps, widely used in off-grid communities, release significant amounts of carbon dioxide and black carbon into the atmosphere.

By displacing these with solar systems, M-KOPA customers collectively reduce greenhouse gas emissions while also avoiding health hazards linked to poor indoor air quality.

Industry reports estimate that M-KOPA’s solutions have already helped avert millions of tons of CO2 emissions, underscoring its role in advancing Africa’s clean energy transition.

Challenges M-KOPA Faced

1. High cost of customer acquisition

Acquiring customers in rural and peri-urban areas is resource-intensive. M-KOPA relies heavily on door-to-door sales agents and local partnerships, which increases upfront costs. While this model helps build trust with communities, the cost of onboarding a new customer often outweighs the initial revenue generated, requiring patient capital to sustain.

2. Loan defaults and repayment risks

M-KOPA’s pay-as-you-go model depends on customers making consistent micro-payments. However, many low-income households experience income fluctuations due to informal or seasonal work. This unpredictability increases the risk of defaults, affecting the company’s cash flow and making it challenging to manage repayment schedules at scale.

3. Balancing social impact with profitability

From the outset, M-KOPA’s mission has been to provide affordable energy and financial services to underserved populations. Yet, achieving this social impact while remaining profitable has been a delicate balance. Keeping payment plans affordable often reduces margins, forcing the company to innovate continuously to maintain sustainability.

4. Complex regulatory environments

Operating across multiple countries—such as Kenya, Uganda, and Nigeria—means navigating diverse regulatory frameworks governing finance, telecommunications, energy, and consumer protection. Shifting government policies, inconsistent enforcement, and bureaucratic hurdles often slow down operations and complicate product rollout.

5. Operational scaling challenges

With millions of customers and thousands of field agents, scaling operations has tested M-KOPA’s efficiency. Training and managing a dispersed workforce, ensuring product delivery to remote areas, and providing timely customer support are ongoing challenges that strain logistics and operations.

6. Criticism on debt stress and repossessions

Some customers and media outlets have raised concerns about the burden of debt associated with M-KOPA’s model. When customers fail to meet repayment obligations, devices may be repossessed or locked remotely. While this protects the company from losses, it has sometimes been perceived as exploitative, raising questions about ethical lending practices in low-income communities.

7. Talent retention and leadership strain

As the company grew rapidly, retaining skilled employees and maintaining strong leadership became crucial. The competitive landscape for talent in Africa’s fintech and energy sectors means M-KOPA has to invest significantly in staff development and incentives. Leadership transitions, particularly during phases of rapid scaling, have also tested organizational stability.

Despite these challenges, M-KOPA has largely managed to keep its customer base growing.

Its accumulated lessons from early missteps (shifting distribution models, engaging communities, adjusting payment plans during income shocks) have improved resilience.

But the risks of over-indebtedness in ultra-poor communities remain an ethical concern. Industry watchers note that any fintech aiming at the poorest must guard against creating new debt traps, even unintentionally.

M-KOPA’s founders and backers have publicly stressed responsible lending (no hidden fees, education for customers) as they scale.

Read Also: Inside Chipper Cash’s Journey: Redefining Cross-Border Payments in Africa

Lessons from M-Kopa’s Journey

M-Kopa’s story offers several broader lessons about scaling inclusive businesses in Africa:

Integrate technology with affordability

M-Kopa’s success hinged on matching sophisticated tech (cloud platforms, IoT meters, data analytics) with ultra-affordable pricing. It showed that innovation must meet customers’ budgets and habits. The lesson: don’t chase trendy technology for its own sake; design it around the end-user.

M-KOPA famously “bucked the conventional box” by inventing a hybrid model. For entrepreneurs, this underscores the need to blend digital solutions with local context – e.g. leveraging prevalent mobile money systems, or tailoring loan terms to the daily-wage cycle.

Leverage patient, impact-oriented capital

Without long-term, mission-driven investors, M-KOPA might never have scaled. Early on, impact backers like LGT and Generation were willing to fund losses as customers grew. Even the Gates Foundation pitched in (via a $5M loan) to demonstrate the viability of asset-backed lending for the poor.

These investors tolerated slow returns while M-KOPA built a massive repayment dataset. The lesson: for deeply inclusive models, patient capital (equity and concessional debt) can bridge the “valley of death” before profitability.

As one founder quipped in 2015, investors still needed convincing that they’d “make money by selling solar to people on $2-a-day” – but the patient capital kept the model alive until it proved out.

Build credit histories through assets

M-KOPA has shown how energy access programs can simultaneously create financial inclusion.

By embedding financing into appliances, it effectively turned each customer into a formal borrower. Creating 75,000+ new credit records by 2016 helped many clients qualify for other services later.

This approach – turning a solar home system into “bankable collateral” – has influenced others in the sector (even competitors license M-KOPA’s PAYG tech).

Policymakers and fintech designers can learn that extending small asset loans (with mobile payback) can pull the unbanked into the formal economy in a way that cash loans alone often cannot.

Scale gradually, then diversify

M-KOPA didn’t start by offering everything at once. Its lesson is to perfect one core product (solar lighting in rural Kenya) and distribution, then gradually add complementary products and services.

By 2019, it had sufficiently served East Africa that it could afford to experiment with phones, then TVs, then microloans and insurance.

This sequential expansion helped it avoid spreading itself too thin. Many newer start-ups have emulated this “start with solar, then branch” playbook (for example, PEG Africa explicitly licensed M-KOPA’s methodology).

Use data wisely, but guard customers

M-KOPA’s data collection has been an advantage: its AI-driven credit scoring (leveraging every micro-payment) allows smarter lending and cross-selling. The lesson is that even “dumb” products can become rich data sources.

However, M-KOPA’s journey also warns that data can be a double-edged sword. While building credit is positive, the company must ensure data analytics don’t inadvertently exclude or penalize vulnerable users.

Its policy of not charging late fees suggests a sensitivity to customer hardship. Balancing growth with fairness is an ongoing lesson: fintech firms must couple data models with empathy.

Impact beyond energy

Finally, M-KOPA demonstrates that clean-energy solutions can catalyze broader development. Its off-grid solar program ended up serving as a gateway to fintech. Millions of Africans now access the internet, make formal payments, and even save through a project that began as a lamp.

This cross-sector impact – from health (by reducing kerosene fumes), to education (lighting for students), to entrepreneurship (refrigerated produce sales) – shows how interconnected development goals can be.

Entrepreneurs and investors should note that solving one problem (electricity access) can unlock others (financial inclusion, women’s empowerment, climate resilience) if approached holistically.

Conclusion

M-KOPA’s 15-year journey highlights the power of aligning business incentives with social needs. Its founders proved that rural Africans can be creditworthy customers when given the right product and payment tools.

The lessons – from marrying finance with energy, to the necessity of patient capital, to leveraging mobile money infrastructure – are now a blueprint for many inclusive ventures. As one of the continent’s largest fintech/asset-finance platforms, M-KOPA’s future looks toward serving millions more.

Its biggest impact may yet lie in showing that sustainable, scalable innovation in Africa must integrate technology with affordability, data with compassion, and profit with purpose.

Leave a comment and follow us on social media for more tips:

- Facebook: Today Africa

- Instagram: Today Africa

- Twitter: Today Africa

- LinkedIn: Today Africa

- YouTube: Today Africa Studio