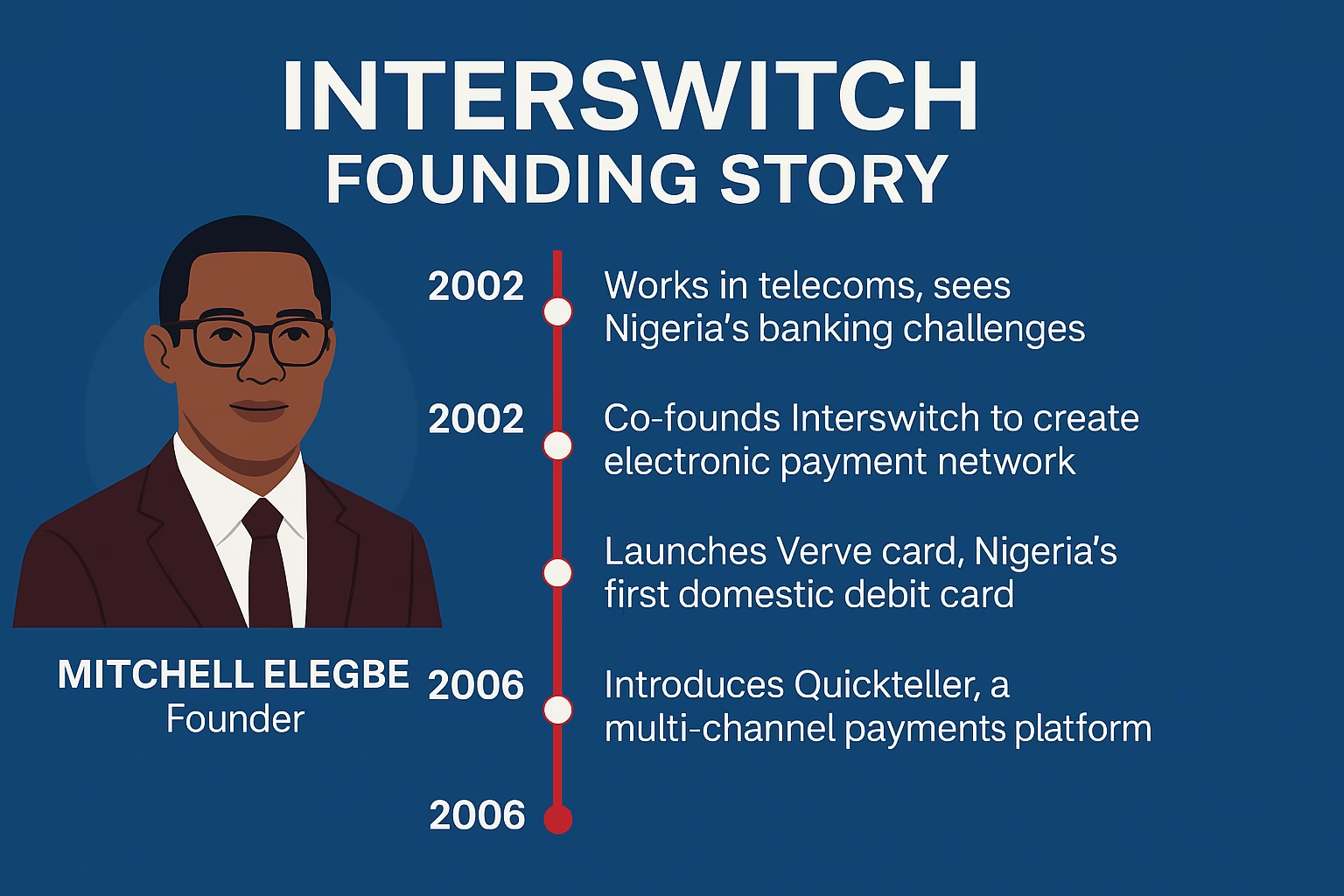

In 2002, long before “fintech” became a buzzword in Africa, one Nigerian engineer saw a broken financial system and envisioned a seamless digital payments network.

That engineer, Mitchell Elegbe, would go on to found Interswitch, the company that built the rails for Nigeria’s electronic payments ecosystem and became a blueprint for homegrown innovation in emerging markets.

At a time when Nigerians endured long bank queues, carried cash across dangerous highways, and operated in a largely unbanked economy, Interswitch offered a bold alternative: a nationwide transaction switching system that would connect banks, ATMs, merchants, and eventually millions of consumers.

Over two decades later, Interswitch is not only Nigeria’s first fintech unicorn, but also a backbone of Africa’s digital economy, processing trillions of naira annually and powering financial inclusion for millions.

This is the inside Interswitch’s journey, a story of how one company reimagined payments in Africa, built the infrastructure others now rely on, and laid the groundwork for a digital financial revolution.

Disclaimer: The data in this episode of StoryLab is based on publicly available funding information as of July 2025 from reliable sources such as Startuplist Africa, TechCabal, TechCrunch, and official press releases.

How Interswitch Started

Interswitch is a Nigerian fintech powerhouse – a payments and commerce infrastructure company founded in 2002 – that helped usher Africa’s move from cash to digital finance.

Founded by Mitchell Elegbe, an electrical/electronic engineering graduate who had worked in telecoms, and fellow technologists.

Elegbe’s inspiration came from witnessing Nigeria’s cash-driven, paper-based banking pains: people stood in Friday queues to withdraw weekend cash, and even highway robberies spiked as unconnected bank branches left customers to carry cash wherever they went.

In 2002, Elegbe left his job at Telnet, rallied support (even from his employer), and co-founded Interswitch with Charles Ifedi to build “Switch” software that would link banks and ATMs together.

With backing from Accenture and early bank sponsors, he and founding colleague Akeem Lawal (later head of switching) set out to digitize Nigeria’s payments.

Interswitch’s name reflects this “switching” mission: it became the highway connecting banks, merchants, and consumers electronically.

Interswitch took on a huge market gap. At inception, over 50% of Nigerians were unbanked or underbanked, and the existing banks had no inter-branch network.

As Elegbe noted, branches “did not have any software connecting them”, forcing Nigerians to withdraw only from their home branches. Cash scarcity and crime were endemic. Interswitch aimed to solve this by creating a country-wide payment backbone.

This founding vision – born of local insight – guided Interswitch’s growth. (Later founders and team members, including Akeem Lawal, had similar tech and engineering backgrounds.)

Milestones in Interswitch’s Journey

Interswitch’s rise has been marked by product launches, strategic partnerships, and several major funding events. Key milestones include:

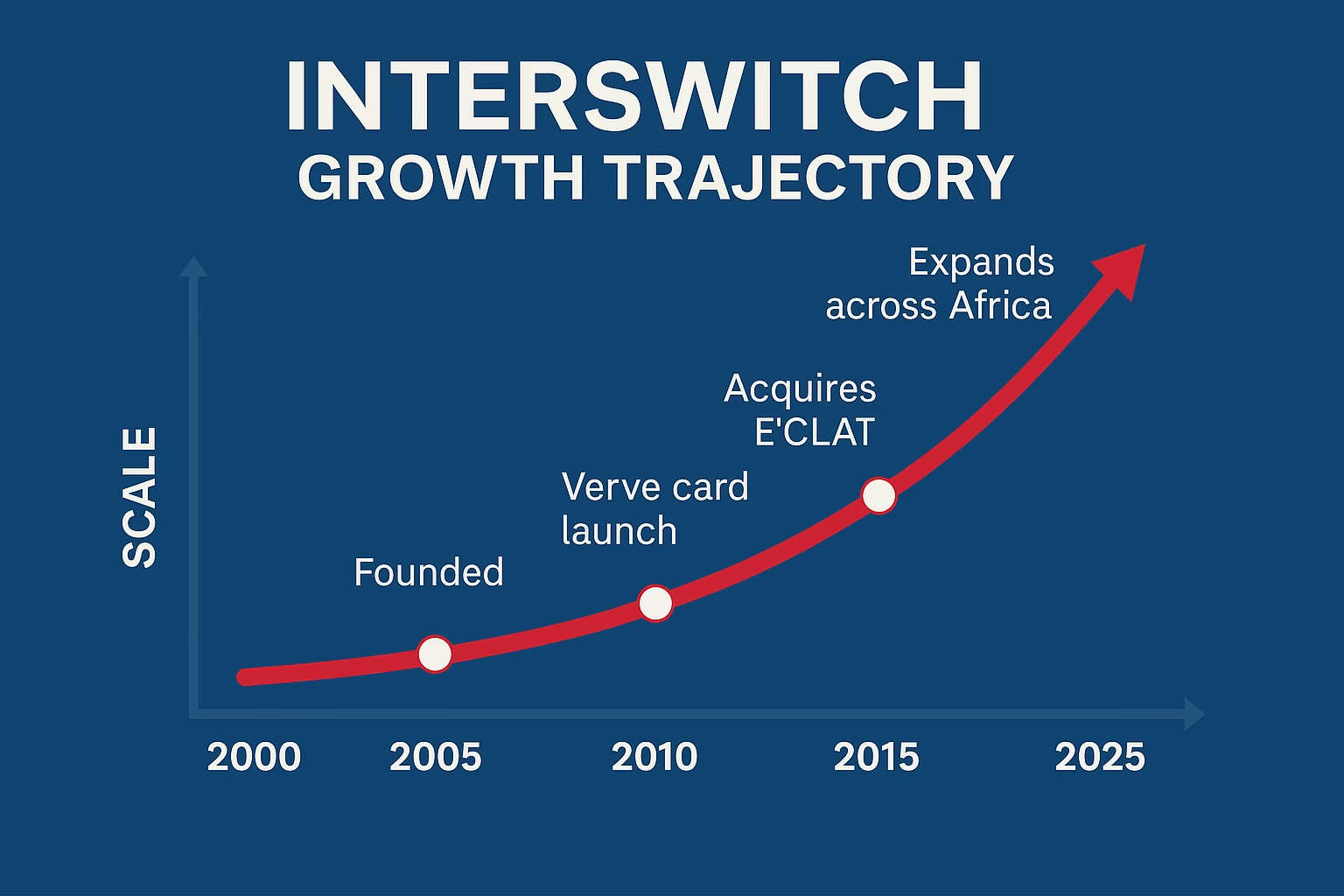

- 2002 – Founded: Interswitch launches its core transaction switching platform in Nigeria, initially connecting a handful of banks’ ATM networks. The first switch connected 7 banks, quickly growing to 13 banks plus an ATM consortium and even Globacom’s mobile money network.

- Mid-2000s – Verve Card: Interswitch introduced Verve, Africa’s first domestic debit card network. By 2013, Verve had 18 million of Nigeria’s 25 million payment cards in circulation, and today it claims ~70% market share of Nigeria’s cards. Verve operates across 21 African countries (and 185 countries worldwide via global schemes), empowering millions of users without relying on foreign card networks.

- 2006 – Quickteller: The company launched Quickteller, a multi-channel payments platform for consumers and businesses. Quickteller aggregated billers and services (hospital bills, utilities, flights etc.), enabling online and mobile payments. Today Quickteller connects 8,000+ billers and supports 41,000+ PayPoint agents nationwide (community vendors who process payments), extending services to rural customers. Quickteller’s evolution includes loans and a “super-app” strategy, and in 2021 it added Quickteller Business to help SMEs manage collections.

- 2010 – Helios Consortium & Bankom: Two-thirds of Interswitch was bought by a consortium led by Helios Investment Partners, giving it new capital and governance. Interswitch then expanded regionally: it took a 60% stake in Bankom (Uganda) to enter East Africa.

- 2013–2015 – Discover Partnership & Paynet: In 2013 Interswitch partnered with Discover Financial Services (USA) to expand acceptance. In 2014 it acquired a majority stake in Paynet Group, an East African payments firm. By 2015 Interswitch was also launching a $10 million African startup fund and acquiring VANSO (a Nigerian mobile banking tech firm) to strengthen its services.

- 2017 – Visa Partnership: Interswitch teamed up with Visa to promote QR/mobile payments (mVisa) regionally. This collaboration paved the way for further investment: in November 2019 Visa invested $200M for a 20% stake in Interswitch. That round valued Interswitch at ~$1 billion and officially made it Nigeria’s first fintech unicorn. Other investors by then included TA Associates, IFC, and local private equity (as noted in press releases).

- 2020 – Debt Listing: Instead of an IPO (see below), Interswitch issued corporate debt. It listed a ₦23 billion bond (about US$63M) on the Nigerian Stock Exchange in Feb 2020, diversifying funding sources.

- 2023 – Record Volumes: In March 2023, Interswitch’s platform hit 1.2 billion transactions in a single month, a 58% jump from the previous month. By contrast, all of 2019 saw just 2.7 billion transactions. This meteoric growth reflects Nigeria’s digital migration (partly accelerated by cash shortages) and Interswitch’s investment in capacity.

Throughout its journey, Interswitch innovated continuously. It launched new services (like Retailpay and Smartgov – an ID/e-payments platform for state governments), built infrastructure (e.g, the “Superswitch”), and grew its Verve and Quickteller networks.

The company also ventured into financial inclusion: in 2015, it created Interswitch Financial Inclusion Services (IFIS), trading as Quickteller Paypoint, a licensed “super-agent” network to deliver digital payments to underserved Nigerians.

Read Also: Inside Moniepoint’s Journey: From POS Terminals to Africa’s Fintech Powerhouse

Interswitch funding history

| Year | Amount Raised | Investor(s) | Notes |

|---|---|---|---|

| 2002 | ~₦200 million (approx. $1.5M at the time) | Telnet Nigeria, Accenture (support), Bank Consortium | Seed funding to build Nigeria’s first transaction switching infrastructure. Backed by Elegbe’s employer (Telnet) and key banks. |

| 2010 | Undisclosed (majority stake acquisition) | Helios Investment Partners | Helios acquired a majority stake (~67%) in Interswitch, marking the first major private equity buy-in. |

| 2016 | $110 million (approx.) | TA Associates, existing shareholders | TA Associates acquired minority stake from Helios. Valued Interswitch at ~$400–500M. |

| 2019 | $200 million | Visa Inc. | Visa acquired a 20% stake, valuing Interswitch at $1 billion (unicorn status). Strategic partnership for card/QR expansion. |

| 2020 | ₦23 billion (~$63 million) | Nigerian Capital Market (Corporate Bond Issuance) | Listed a ₦23B bond on the Nigerian Stock Exchange to diversify capital sources. |

| 2023 | Undisclosed (Internal reinvestment + debt) | Internal profits + Debt Investors | No major external equity round; company funded expansion from retained earnings and minor debt refinancing. |

Strategies Fueling Growth

Interswitch’s scale comes from deep partnerships, technology infrastructure, and wide distribution. Key strategic elements include:

1. Bank and institutional partnerships

From the start, Interswitch worked with banks as partners. Early backers included TELNET (Elegbe’s employer), GTBank, and others. It later partnered with Nigeria’s Central Switch (NIBSS) and regulators to become the rails for ATM/POS transactions nationwide.

Government partnerships also grew: by the 2010s, Interswitch ran payment systems for many state governments (via Smartgov) and was recently approved as a pension payments provider in 2025.

2. Agent network (Quickteller PayPoint)

To reach the unbanked, Interswitch deployed agents in communities. Its Quickteller PayPoint network now has 41,000+ local payment agents in Nigeria. This allows people with no bank account or smartphone to pay bills, make deposits, or withdrawals through trusted neighborhood businesses.

(Interswitch touts this as “the interconnect point” for financial inclusion.) The agent model helped Interswitch acquire customers in peri-urban and rural areas faster than branch expansion alone.

3. Technology and reliability

Interswitch invested heavily in a robust platform. Its core switching system (branded “Superswitch”) was built for high throughput and 99.9% uptime, giving banks confidence to migrate their transactions.

It integrated with global card schemes (Visa, Mastercard, Discover) and built a scalable payment gateway for online merchants. During Nigeria’s 2023 cash crunch, CEO Elegbe noted that Interswitch’s technology “provided much-needed relief” by enabling digital transactions at scale.

4. Consumer and SME apps

While Interswitch started B2B, it didn’t ignore end-users. The Quickteller app (launched in 2010s) and Verve cards aimed at consumers and small merchants. For businesses, the Quickteller Business app (2021) and API gateway enabled merchants to accept payments.

These channels expanded Interswitch’s footprint beyond banks into e-commerce, retail and utility payments. Notably, Quickteller now has 8,000+ billers connected and 190,000 active businesses making payments on it daily.

5. Acquisitions & investments

Interswitch bought or invested in complementary fintechs (e.g., VANSO, Paynet, etc) and set up a venture fund (2015) to invest in early-stage African payments startups. This both expanded their portfolio and kept them in touch with innovation.

For example, acquiring Paynet (East Africa) and Bankom (Uganda) gave Interswitch cross-border reach. Partnerships with telcos (like Globacom) and Visa likewise extended services (e.g., mobile payments).

6. Regulatory navigation

Interswitch worked closely with regulators. It helped modernize Nigeria’s payment rules (e.g. inter-switch regulations) and used its scale to standardize electronic payment security. When others struggled with licensing, Interswitch leveraged its early-in market advantage.

It even considered listing publicly multiple times but chose to wait out unfavorable economic conditions (2016 recession, then COVID). Its 2020 bond issuance was one way to fund growth while equity markets were unsettled.

These strategies created network effects: more banks and merchants attracted more consumers and agents, which in turn made Interswitch indispensable.

Today, its payments infrastructure processes trillions of naira each year, with the company reporting ~190,000 Nigerian businesses transacting daily on its platform.

See Also: Top 14 Angel Investors Funding African Startups

Competition in the Fintech Ecosystem

By the 2010s, newer fintech startups challenged Interswitch in Nigeria’s digital payments space. Each has its own niche and approach:

1. Flutterwave (2016)

Flutterwave was co-founded by Iyinoluwa Aboyeji and Olugbenga Agboola in 2016. Initially, Aboyeji served as CEO, but later stepped down, and Olugbenga Agboola assumed the CEO role.

A Nigerian startup focusing on cross-border and online merchant payments via APIs. Flutterwave grew rapidly, raising ~$475M by early 2022 and achieving a ~$3B valuation. It serves major global clients (Uber, Booking.com), supports payments in 150 currencies, and processes ~200M transactions worth $16B annually.

Unlike Interswitch’s bank-centric model, Flutterwave targeted tech startups and e-commerce with easy integration. It also introduced consumer apps (Barter) and remittances (Send). In essence, Flutterwave captured the online SME market that Interswitch’s more corporate infrastructure did not initially serve.

2. Paystack (2015)

Paystack was co-founded by Shola Akinlade and Ezra Olubi. They are both Nigerian computer science graduates who created Paystack to simplify online and offline payments for businesses across Africa.

A Lagos-based payments API service for local businesses. Paystack built a simple checkout solution for merchants and, by 2020, had about 60,000 business customers. It was acquired by Stripe in late 2020 for over $200M. Paystack’s success lay in developer-friendly tools and integration with banks.

After the Stripe deal, it continued serving Nigerian and African merchants independently. Paystack’s model contrasted with Interswitch by being exclusively online-focused (no own card network) and aggressively pursued small and medium enterprises.

3. Paga (2009)

Tayo Oviosu is a Nigerian-American businessman who is the founder and group CEO of Paga, a mobile payments company that is focused on digitizing cash in emerging economies.

Paga is a mobile money platform built around agents and mobile apps. It enabled peer-to-peer transfers, bill pay, and merchant services via mobile wallets. As of 2024, Paga reported 23 million users and had processed ~335 million transactions totaling ~$32B.

Paga focused on unbanked rural customers through a vast agent network. In comparison, Interswitch built a universal network (bank, card, utility) but later expanded to similar agent-based reach via Quickteller PayPoint.

4. Chipper Cash (2018)

A pan-African app for free P2P and cross-border transfers. Founded by Ham Serunjogi and Maijid Moujaled, Chipper Cash raised ~$152M by mid-2021 (including a $100M Series C) and grew to ~4 million users across 7 African countries and the UK.

It showed the appeal of mobile-first, consumer-oriented fintech. Unlike Interswitch’s enterprise focus, Chipper went after individuals sending money across borders. (Chipper also ventured into crypto, illustrating a newer fintech trend Interswitch has largely steered clear of.)

See Also: How to Legally Protect Your Startup Idea in Africa

Comparative Funding of Interswitch vs Peers

This compares Interswitch’s funding to other African fintech giants:

| Company | Founded | Total Funding | Key Investors | Latest Valuation | Focus |

|---|---|---|---|---|---|

| Interswitch | 2002 | ~$400M+ (Equity + Debt) | Helios, TA Associates, Visa | ~$1.2B (2023 est.) | Payments infrastructure, card network, B2B |

| Flutterwave | 2016 | ~$475M | Tiger Global, Greycroft, Green Visor | ~$3B (2022) | Payment API, cross-border merchant services |

| Paystack | 2015 | ~$10M (pre-exit) | Stripe (acquired), Visa | ~$200M (2020 acquisition) | SME-focused payment API |

| Paga | 2009 | ~$35M+ | Goodwell, Omidyar, Adlevo Capital | Private (~$200–250M est.) | Mobile money, agent networks |

| Chipper Cash | 2018 | ~$300M | SVB Capital, FTX Ventures, Ribbit Capital | ~$2B (2021, unicorn) | Cross-border P2P transfers, crypto, wallets |

Each competitor found growth by targeting niches that Interswitch didn’t initially occupy: online businesses, peer-to-peer remittances, and wallets. Interswitch, in turn, responded by broadening its services.

Its Quickteller app and Verve cards competed for consumer attention, while its underlying platform served fintechs (Flutterwave and Paystack rely on Interswitch rails in Nigeria).

The presence of these players highlights Nigeria’s vibrant payments landscape: Flutterwave and Paystack enabled online commerce, Paga and Chipper expanded mobile payments, while Interswitch anchored the national infrastructure.

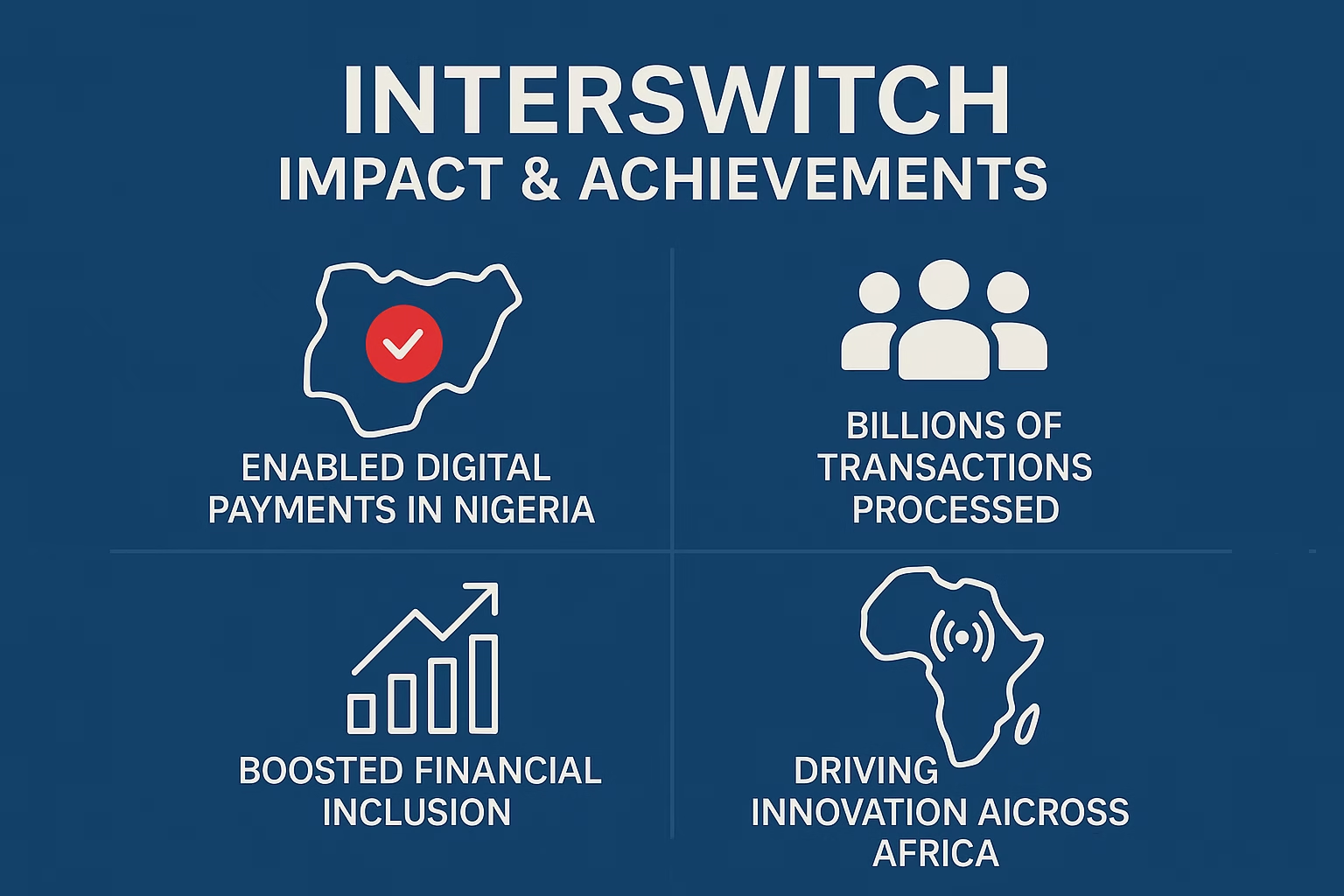

Impact on Financial Inclusion

Interswitch’s impact on inclusion is significant. By creating interoperable payment rails and a ubiquitous agent network, it brought millions of Nigerians into the digital economy. For example, its Quickteller PayPoint agents have reached rural areas where no banks exist.

Verve cards and QR/mobile payments let people use bank-like services without visiting a branch. In the recent naira redesign crisis, Interswitch’s technology allowed many citizens to avoid cash hoarding by paying businesses and bills digitally – a relief noted in their own reports.

Quantitatively, Interswitch reports 190,000 businesses transacting daily on its platform and 70 million Verve cards activated. These numbers illustrate its breadth: from city fintech startups to village retailers.

It also underpins Nigeria’s move toward inclusion: the Central Bank of Nigeria has cited the growth of electronic payments (now about a third of transactions) as a national goal.

Interswitch, as the plumbing behind ATMs, POS, and e-bills, has therefore played a backbone role in that goal.

Challenges and Recent Developments (2020s)

Despite its successes, Interswitch has faced challenges. Economic and regulatory headwinds in Nigeria have delayed its IPO ambitions. Plans for a dual listing (London/Nigeria) first floated in 2016 stalled in recession.

Even after COVID-19, an IPO has remained uncertain, as one CEO memo noted that listing would happen “when private equity investors want an exit”.

Meanwhile, competition has intensified: mobile money and fintech apps (eNaira, and private apps) have chipped away at traditional models, forcing Interswitch to innovate (e.g. adopting contactless, QR, loyalty programs).

As of 2025, Interswitch is still a giant in Nigeria. It processes roughly 90% of the country’s electronic payment transactions, giving it huge influence over pricing and standards.

It has expanded in East Africa (Kenya, Uganda) and West Africa (Ghana, The Gambia) in partnership with local banks and telecoms. Recently, it launched a multi-currency prepaid card in Kenya and unveiled a global payments innovation report with the World Bank.

These moves show Interswitch positioning itself as a pan-African platform leader.

However, Interswitch’s size also means it must adapt more carefully. Some analysts note that its dominance could slow responsiveness to new trends (e.g. cryptocurrencies, open banking) compared to scrappier startups.

And Nigeria’s macro troubles (inflation, foreign exchange shortages, policy shifts) continue to pressure revenues. Internally, the company has reinvested capital – not paid dividends – to stay nimble.

It is also quietly building “super-app” features into Quickteller to compete with all-in-one wallets (like OPay, another Nigerian fintech) while leveraging its core strength in secure payments.

Why Interswitch Succeeded – Lessons Learned

1. Solving real pain points

Solving real pain points at the right time was crucial: it built the first nationwide electronic payments infrastructure when none existed. Mitchell Elegbe often emphasizes that “solving big problems” leads to big rewards.

By focusing on interoperability (versus creating yet another closed mobile money silo), Interswitch became the trusted rails for the financial system. This first-mover advantage was durable; even as new apps emerged, they often plugged into Interswitch’s network.

2. Building ecosystems and partnerships

Interswitch didn’t try to go it alone; it worked with banks, governments, and global players like Visa. Early buy-in from banks (e.g. $10 million investments yielding N2.6 billion in value for some shareholders) showed how aligning incentives can pay off.

Interswitch also invested in adjacent businesses (e.g. its $10M fund and tech acquisitions) to stay relevant. Lesson: incumbents should invest in the broader ecosystem rather than fending off startups alone.

3. Patience and persistence

Interswitch spent years developing its core before exploding in value. It delayed chasing short-term profits to reinvest and waited for an IPO only when conditions were right. According to Moody’s, Interswitch now holds 90% market share in switching – a reward for steady scaling. Prospective founders can learn that building infrastructure is slow but can yield monopolistic positions.

4. Local insight and culture

This gave Interswitch an edge. It tailored solutions to Nigeria’s reality: agent networks addressed cash transactions; Verve cards worked with chip-and-PIN in local currency; payment services often operate offline or via SMS for poor internet conditions.

International fintech models often misfire without localization. Interswitch’s in-depth understanding of Nigeria’s challenges (from road travel to rural billing) allowed it to design sticky solutions.

However, Interswitch’s journey also warns of complacency. In a fast-moving tech field, former giants can be leapfrogged by innovation.

Interswitch must continue to innovate – for example, by making Quickteller more than a payments app, or by exploring emerging sectors (insurtech, blockchain IDs, etc.).

The unfulfilled IPO also shows that success in private markets doesn’t guarantee public market readiness; managing investor expectations and economic cycles is crucial.

Read Also: 20 Most Funded Startups in Africa Still Active This Year

Interswitch in Today’s Fintech Industry

Today (2025) Interswitch stands as one of Nigeria’s most important fintech companies. It pioneered the electronic payments era in Nigeria and remains deeply embedded in daily life.

Its achievements – first fintech unicorn, billions in monthly transactions, and an unrivaled payments network – have cemented its legacy.

Yet the ecosystem has grown richer. Startups like Flutterwave and Paystack have taken inspiration from Interswitch’s infrastructure, and now serve the merchant and tech startup segment. Consumer fintechs like Chipper and Paga have broadened finance for individuals.

Interswitch’s current strategy is to leverage its scale: it is positioning Quickteller as a mini-superapp (broader lifestyle services), exploring strategic partnerships (blockchain and AI initiatives), and preparing for further African expansion (potentially via IPO or acquisitions).

Conclusion

From a Nigerian market perspective, Interswitch is a textbook case of homegrown innovation solving local needs and then scaling globally.

Its impact on financial inclusion is profound – it literally “changed the way Nigerians pay and get paid” – and its brand is a household name.

Its success factors – starting with a clear problem, building reliable tech, partnering with incumbents, and reinvesting for growth – offer a roadmap for other entrepreneurs.

Interswitch shows that by solving real problems in emerging markets with persistence and partnership, a startup can grow into a regional powerhouse.

As Nigeria and Africa digitize further, Interswitch is likely to remain a central pillar of that ecosystem, even as it adapts to new challenges and competition in the years ahead.

Leave a comment and follow us on social media for more tips:

- Facebook: Today Africa

- Instagram: Today Africa

- Twitter: Today Africa

- LinkedIn: Today Africa

- YouTube: Today Africa Studio