Inside M-Pesa’s journey lies one of the most remarkable stories of technological innovation reshaping the financial industry of Africa and beyond.

Launched in Kenya in 2007 by Safaricom and Vodafone, M-Pesa (short for “mobile money” in Swahili) emerged as a bold experiment to address the limited access to banking services in developing economies.

What began as a donor-funded pilot project aimed at facilitating microfinance repayments rapidly evolved into a revolutionary mobile money platform, enabling millions to send, receive, and store money using only a basic mobile phone.

Over the past decade and a half, M-Pesa has transformed from a simple SMS-based service to a multifaceted digital ecosystem, powering payments, savings, credit, and commerce for over 50 million users across Africa.

This analysis traces M-Pesa’s founding story, growth trajectory, and societal impact, explores its competitive industry and global expansion efforts, and examines the key lessons it offers to others.

Disclaimer: The data in this week episode of StoryLab is based on publicly available funding information as of July 2025 from reliable sources such as Startuplist Africa, Tech Safari, Techpoint Africa, TechCrunch, and official press releases.

Founding Story

In 2005, Safaricom – Kenya’s largest mobile operator, part-owned by Vodafone – secured a grant from the UK’s Department for International Development (DFID) to pilot a mobile-based microfinance platform.

Vodafone engineers and Safaricom executives, led by visionaries like Michael Joseph and Nick Hughes, discovered in early trials that rural Kenyans were using the system not for loans but for person-to-person transfers.

They quickly pivoted the project to focus on remittances and simple payments. In March 2007, following this donor-funded pilot, Safaricom formally launched M-PESA (short for “mobile pesa,” Swahili for money) as an SMS-based money-transfer service.

Users could deposit cash with local “M-PESA agents,” send e-money via SMS, and withdraw cash at any other agent – all without a bank account.

Safaricom had obtained a “letter of no objection” from the Central Bank of Kenya, creatively structuring M-PESA as an e-money vault in partnership with banks rather than a full banking license.

Kenya’s reliance on cash and limited rural banking made the product an instant hit. Contrary to industry expectations, the adoption exploded.

Safaricom had conservatively aimed for 350,000 users in the first year, but by November 2007, M-PESA was serving over 1.04 million active users – far surpassing targets.

By late 2009, according to economists Jack and Suri, some 7.7 million accounts were registered with over 23,000 agents, and more than two-thirds of Kenyan households had at least one M-PESA user.

Michael Joseph recalls that the concept was initially met with skepticism by some, but “M-Pesa’s ease of use and convenience quickly won over users,” leading to viral growth.

As Vodafone later summarized, M-PESA “spread quickly” and became “one of the most successful mobile-phone–based financial services in the developing world”.

By late 2007, just months after launch, average new registrations hit nearly 10,000 per day. Within a decade, it would grow into a platform with tens of millions of users and hundreds of thousands of agents across multiple countries.

Expansion

Initially available only in Kenya, M-PESA soon expanded to Safaricom’s partner markets. Vodacom (Vodafone’s Africa affiliate) launched it in Tanzania in 2008, and later rolled it out in Ghana, Mozambique, Lesotho, the Democratic Republic of Congo and Egypt.

Vodafone India (in partnership with ICICI Bank) introduced M-PESA in 2011-13, and Vodafone Romania debuted it in 2014.

However, some international pilots faltered: the India and Romania ventures were later wound down due to stiff competition and regulation. (For example, Vodafone Romania’s launch in 2014 marked the first European M-PESA service, but it never gained large-scale.)

In contrast, M-PESA by 2015 had penetrated nearly every segment of Kenyan life, from urban centers to remote villages. Vodafone’s own press noted that within Kenya, the system had achieved near-ubiquity, processing 6 billion transactions a year by 2016.

As Michael Joseph later reflected, “M-PESA is a revolution that has empowered tens of millions of people in some of the poorest communities in the world”.

Indeed, by 2025 it was celebrated as Kenya’s “leading financial platform,” with 34 million Kenyan users – over two-thirds of the population – relying on it for payments, remittances, and savings.

Funding History

The initial funding for M-PESA was modest but critical. Safaricom and Vodafone invested roughly £2 million (about USD $3 million) to build the prototype, comprised of a £1 million DFID grant and £1 million from Vodafone.

These seed funds paid for technology development, marketing, and agent recruitment. The early venture benefited from donor support (notably the UK Government and later the Bill & Melinda Gates Foundation via GSMA) and was managed internally within Safaricom/Vodafone’s product budgets.

There were no traditional venture-capital rounds; instead, Safaricom’s broader investments in network infrastructure and corporate financing indirectly fueled M-PESA’s growth.

For example, Safaricom’s 2008 IPO (Kenya’s largest ever) and subsequent capital raises provided ample resources for scaling networks and systems.

Over time, strategic partnerships supplemented funding and capability. Vodafone rebranded M-PESA as a global technology platform, providing expertise and funds for new markets.

For instance, in 2010, Vodafone invested in the launch in India (via a partnership with ICICI Bank) and in 2014 backed the Romania rollout.

International aid also played a role: the Gates Foundation, through GSMA’s Mobile Money for the Unbanked initiative, committed $12.5 million to support projects like Roshan’s M-Paisa in Afghanistan.

This grant (2010) helped build the mobile-payments rails in very challenging environments.

In subsequent years, GSMA and other donors funded studies, interoperability work, and financial literacy campaigns around M-PESA, but the core service was largely self-financed by its parent companies.

A major strategic shift came in April 2020, when Safaricom (Kenya) and Vodacom (South Africa) created a joint venture and acquired the M-PESA brand from Vodafone.

This $1.2 billion deal (involving a share swap and cash) consolidated M-PESA’s ownership under the Africa-focused JV, freeing it from Vodafone’s direct management. The purpose was to accelerate expansion across Africa.

At that time, Vodafone noted M-PESA had 40 million users across seven countries and processed over 1 billion transactions per month. The JV’s funding would prioritize technological upgrades, agent growth, and new services (e.g., expanding into Ethiopia and exploring Nigeria).

Overall, M-PESA’s funding “rounds” have been unusual: rather than raising equity from outside, it has leveraged corporate capital from its telecom parents, development grants for pilot projects, and reinvested profits.

Each infusion of support – from the DFID grant in 2005 to Vodafone’s 2020 JV buy-in – corresponded to a clear goal: building the platform, scaling nationwide distribution, and then replicating success regionally.

See Also: Inside Interswitch’s Journey: From Pioneering Payments to Shaping Africa’s Fintech Future

TL;DR: Funding history

| Year | Investor(s) | Funding Amount (USD) | Purpose |

|---|---|---|---|

| 2005 | Vodafone, UK’s DFID (Department for Int’l Development) | ~$3 million (approx. £2 million) | Funded M-PESA pilot project in Kenya; developed initial platform and agent model. |

| 2007 | Safaricom (internal capital) | Not disclosed | Commercial launch in Kenya; marketing, agent network expansion, and system scaling. |

| 2008 | Safaricom IPO (raised ~$840 million total) | Portion allocated to M-PESA (undisclosed) | Funded infrastructure upgrades to handle rapid user adoption and additional agent network growth. |

| 2010 | Vodafone, ICICI Bank (India) | Not disclosed | Launch of M-PESA India pilot and scaling in Tanzania and Afghanistan. |

| 2010 | Bill & Melinda Gates Foundation (via GSMA MMU program) | $12.5 million | Supported M-PESA deployments in challenging markets (e.g., Afghanistan) and interoperability initiatives. |

| 2014 | Vodafone | Not disclosed | Launch of M-PESA in Romania and scaling operations in Mozambique, Ghana, and other African countries. |

| 2020 | Vodacom & Safaricom JV acquisition of M-PESA brand from Vodafone | ~$1.2 billion | Consolidated African ownership of M-PESA platform; focus on innovation and expansion in Ethiopia/Nigeria. |

| 2021–2024 | Safaricom internal investment | Not disclosed | M-PESA Ethiopia launch, smartphone app development, and partnerships for merchant/SME ecosystems. |

Strategies Fueling Growth

1. Agent network

Agent network is one of the key strategies that underpinned M-PESA’s meteoric adoption. Instead of relying on bank branches, Safaricom recruited thousands of local shopkeepers and kiosks as M-PESA agents.

Every village and urban neighborhood soon had an outlet where people could deposit or withdraw cash for their mobile account. Safaricom carefully expanded agents in tandem with users, targeting roughly 1,000 transactions per agent per month, to avoid liquidity shortages.

This decentralized network effectively put “a bank on every corner.” Figure: A M-PESA agent kiosk in Kibera, Nairobi’s largest slum. Agents like this one enabled Kenyans to deposit, send, and receive cash without a bank branch.

The agent strategy was hugely impactful: studies show users are 10–15 minutes’ walk from an agent in Kenya, drastically increasing usage.

2. Affordable pricing

Affordable pricing was another core tactic. Safaricom set very low fees for sending money – especially small amounts – knowing that cost would drive uptake among the poor.

Early on, many transactions under 1,000 KSh ($10) were free or only a few cents. This undercut expensive informal options (like hiring a courier) and made M-PESA irresistible for micro-payments.

In response, competitors like Airtel Money often offered promotions and fee rebates – a recognition of how powerful low pricing was in this market. By keeping costs transparent and low, M-PESA tapped the mass market.

The value proposition – “send money home for less than the price of an SMS” – became part of Safaricom’s marketing, stressing both simplicity and economy.

3. Mobile penetration

Safaricom also leveraged Kenya’s already-high mobile penetration. By 2007, a majority of Kenyan adults had basic cell phones, even in rural areas. M-PESA used this widespread reach: no smartphone or Internet was needed, just an SMS-capable handset.

Safaricom educated its existing prepaid subscriber base (then ~6 million) about mobile money, effectively bundling M-PESA into its core offering. Cross-promotion (e.g. phone top-up with M-PESA) boosted early registrations.

Moreover, Safaricom’s “cool” brand helped: many Kenyans trusted and liked Safaricom, and the green-white M-PESA logo became synonymous with convenience.

4. Strategic partnerships and ecosystem building

Safaricom formed alliances with banks, billers, and governments to make M-PESA truly useful. In 2012, it teamed up with Commercial Bank of Africa to launch M-Shwari, a mobile savings-and-loans product, enabling users to earn interest and take microloans via their M-PESA balance.

In 2019, it added Fuliza, an overdraft feature that lets customers complete payments even if their balance is insufficient.

Safaricom also integrated M-PESA with major utility providers (for bills), merchants (Lipa na M-PESA payments), and e-commerce platforms, ensuring one could pay virtually any Kenyan vendor or utility by mobile.

The government even adopted M-PESA for services like land rent payments and subsidies, further entrenching its use. Crucially, M-PESA targeted the unbanked.

All registration was simple: just an ID, no minimum balance. This inclusiveness meant the poorest Kenyans – many of whom lacked any formal bank, adopted mobile money as their primary financial tool.

In summary, M-PESA’s growth strategy was multi-pronged: build ubiquitous cash-access points through an extensive agent network; price services cheaply; ride on Safaricom’s massive customer base; and create a wide ecosystem of services to make the wallet indispensable.

These tactics created a virtuous cycle: more users attracted more merchants and services, which in turn drew even more users.

As Vodafone’s CEO Nick Read later noted, “M-PESA is hugely successful and enables millions of unbanked people in Africa to transfer money, pay bills, and trade. It benefits communities and helps create a multitude of small and micro-business ventures.”

Competition in the Fintech Ecosystem

M-PESA has remained the dominant mobile money platform in Kenya and much of East Africa, despite facing growing competition over the years. However, most challengers have struggled to meaningfully dent its market share.

Kenya

In Kenya, the most serious competitors to M-PESA have come from other telecom-backed mobile money services:

- Airtel Kenya launched Airtel Money (later merged with Tigo Pesa) with aggressive fee waivers and promotional offers.

- Telkom Kenya introduced T-Kash, and Equity Bank followed with Equitel, a mobile banking service targeting the same market.

Despite these efforts, none came close to dethroning M-PESA. Safaricom’s first-mover advantage, wider agent network, and superior mobile coverage helped it retain a commanding lead.

Note: M-PESA’s dominance is gradually decreasing while Airtel Money is gaining ground. M-PESA’s market share has dropped to 90.8% in Q1 of 2025, while Airtel Money has increased its share to 9.1%. This shift is attributed to Airtel Money’s aggressive promotions, lower fees, and a growing agent network.

Even after Kenya enforced mobile money interoperability in 2018—allowing users to send money across different networks—M-PESA’s dominance persisted.

While some competitors and observers have raised concerns over anti-competitive behavior, Safaricom has denied such claims. Regardless, its market scale remains unmatched.

Other African markets

Outside Kenya, M-PESA’s success has varied:

- Tanzania: Vodacom’s M-PESA leads, competing primarily with Tigo Pesa (Airtel) and MTN Mobile Money.

- Francophone Africa: Safaricom and Vodafone have limited presence. Instead, Orange Money and MTN Mobile Money dominate.

- Ghana and Egypt: Vodafone operates mobile money services, but M-PESA-style dominance is lacking.

Failures in India, Romania, and South Africa

M-PESA’s global expansion has not always succeeded:

- India, Romania, and Albania: Pilot programs were eventually shut down due to regulatory barriers, entrenched financial institutions, and a lack of customer incentives.

- South Africa: Launched in 2010 but discontinued by 2016 after failing to gain traction against MTN’s MoMo and strong traditional banks.

These cases reveal that M-PESA’s model does not easily replicate in environments where formal banking is widespread or regulations are less supportive of telecom-led finance.

Why M-PESA still leads

M-PESA’s sustained success comes down to a few key factors:

- A massive agent network that ensures availability even in remote areas.

- Deep integration into the daily financial lives of users—sending money, paying bills, accessing loans.

- Early adoption created strong network effects, making it harder for competitors to attract new users.

While new fintech players like Wave (West Africa), Paga (Nigeria), and various crypto-based wallets are growing, none have achieved the same ubiquity as M-PESA in East Africa.

Even regulatory efforts such as mobile transaction taxes or transaction limits in Kenya haven’t significantly weakened its grip.

As one analyst put it: “Safaricom’s M-PESA takes the lion’s share of payment services channels in Kenya.”

Despite ongoing innovation in fintech, M-PESA’s position at the center of East Africa’s financial ecosystem continues to shield it from most threats.

Read Also: Inside Moniepoint’s Journey: From POS Terminals to Africa’s Fintech Powerhouse

M-PESA competitive scene

| Country/Region | Main Competitors | M-PESA Market Share / Position | Competitive Dynamics |

|---|---|---|---|

| Kenya | Airtel Money, Telkom’s T-Kash, Equitel | 🟢 96.5% market share (2023) | M-PESA dominates due to first-mover advantage, massive agent network, and brand trust. |

| Tanzania | Tigo Pesa, Airtel Money, MTN | 🟢 Market leader (≈42%) | Intense competition but M-PESA holds largest share due to Vodacom’s strong presence. |

| Uganda | MTN MoMo, Airtel Money | 🟡 Minor player | MTN leads; M-PESA entered late via regional interoperability; limited influence. |

| Rwanda | MTN MoMo, Airtel Money | 🔴 Not present | No direct M-PESA operation; MTN and Airtel dominate mobile money market. |

| Ghana | MTN Mobile Money, AirtelTigo Money | 🟡 Present but not leading | MTN MoMo has strong lead; Vodafone Ghana’s M-PESA has low market penetration. |

| South Africa | MTN MoMo, Nedbank, Banks | 🔴 M-PESA shut down in 2016 | Couldn’t gain traction in highly banked, regulated market with advanced competitors. |

| Nigeria | Paga, Opay, PalmPay, MTN MoMo | 🔴 Not active (as of 2025) | Heavily competitive fintech space; regulation delayed M-PESA entry. |

| Ethiopia | Telebirr (Ethio Telecom) | 🟡 New entrant (launched 2023) | M-PESA growing fast (2.8M users in year one), but faces strong state-backed rival. |

| India | Paytm, PhonePe, Google Pay, Banks | 🔴 M-PESA shut down in 2017 | Regulatory restrictions, strong local competition, and lack of traction led to exit. |

| Romania | Banks, local fintech apps | 🔴 M-PESA shut down in 2016 | Failed to scale; well-banked population preferred card-based solutions. |

| Afghanistan (M-Paisa) | Roshan (Vodafone), local banks | 🟡 Strong niche success | Used mainly for salary disbursement and aid; limited commercial traction. |

Impact on society

1. Mobile money and financial inclusion in Kenya

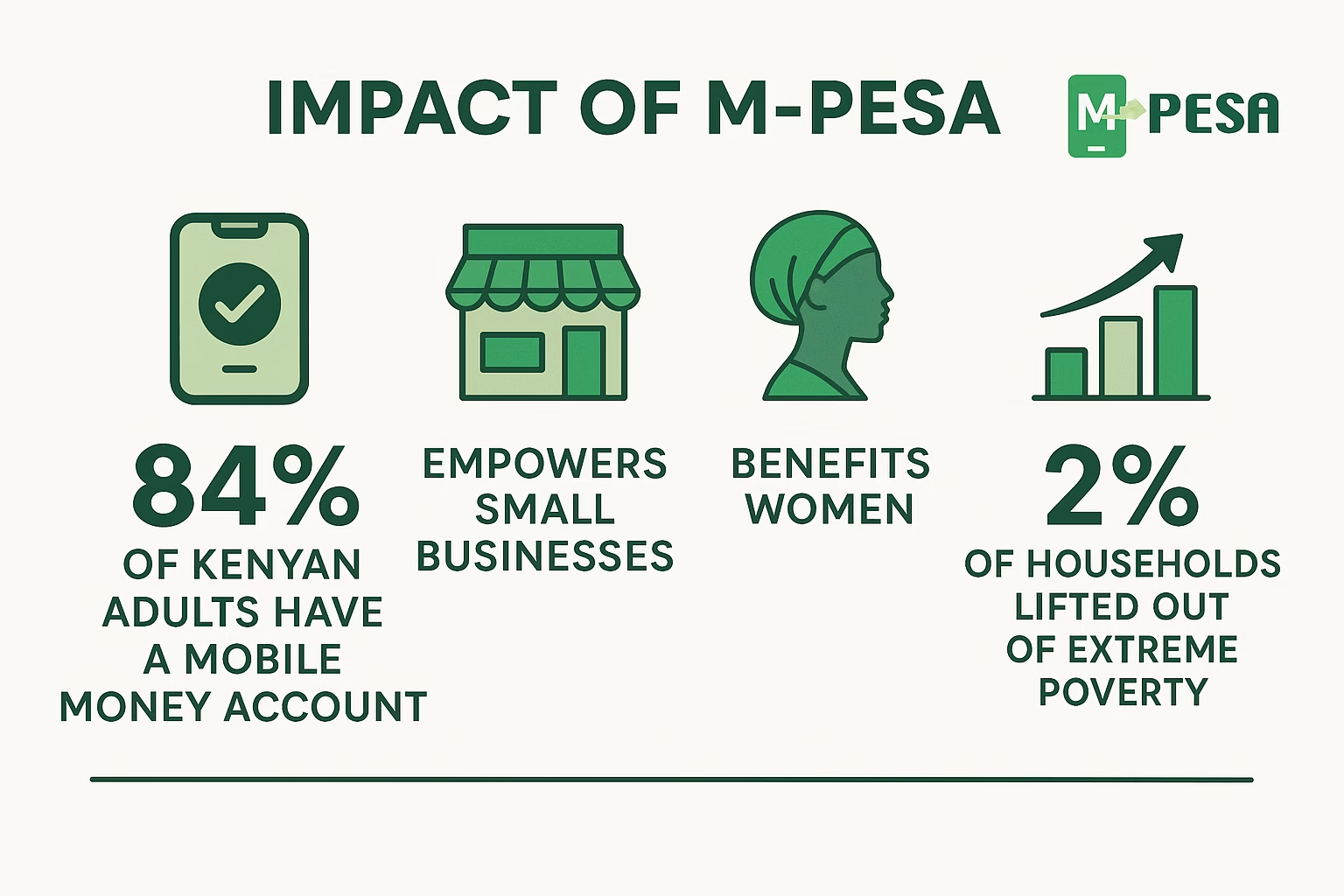

M-PESA has dramatically transformed financial inclusion in Kenya. By 2014, 58% of Kenyan adults had a mobile money account, surpassing the 55% with a traditional bank account. For rural and underbanked populations, M-PESA was revolutionary. It eliminated the need for long treks to banks or reliance on informal cash carriers—money now moved instantly via mobile phones, bringing millions into the financial system.

2. Reducing poverty through access to finance

A study by IPA/J-PAL found that mobile money significantly increased per-capita consumption and lifted 194,000 households (around 2% of Kenyan families) out of extreme poverty. By enabling people to manage income volatility and risk more effectively, M-PESA allowed thousands to climb out of poverty, particularly in rural and vulnerable communities.

3. Empowering women and advancing gender inclusion

M-PESA’s impact on women has been especially profound. It’s estimated that 185,000 Kenyan women transitioned from subsistence farming to small business or trading, enabled by access to capital and mobile markets (poverty-action.org).

By 2021, 66% of Kenyan women owned a mobile money account, compared to just 45% with a bank account (World Bank), showing mobile money’s gender-inclusive potential. Women-headed households, often excluded from formal finance, have particularly benefited.

4. Boosting entrepreneurship and small business growth

M-PESA has become essential for entrepreneurs, vendors, taxi drivers, and small farmers. It allows them to send money home, receive payments, and buy supplies without physical cash. Farmers use it to receive instant payments, helping them secure better prices. Vodafone research suggests that a 10% increase in mobile penetration could raise GDP by 1.2%, a benefit clearly seen in Kenya’s digital economy.

5. M-PESA as a tool for governance and anti-corruption

M-PESA’s utility extends beyond commerce into governance. The Kenyan government and NGOs use it to distribute aid and pay civil servants, reducing corruption and improving transparency.

In Afghanistan, M-Paisa was used to pay police officers and aid workers, dramatically cutting salary theft by local powerbrokers. These examples show M-PESA’s role in building accountable institutions.

6. Universal access and everyday integration

Today, 96% of Kenyan households have access to an M-PESA agent, making it a ubiquitous part of daily life.

Safaricom highlights how users pay school fees, save earnings from fishing, and build savings via M-Shwari—all through mobile phones.

In Safaricom’s words: “A mobile phone is a bank account, the front door to a micro-business, a gateway to higher market prices, or a lifeline for an isolated village.”

See Also: 16 Crowdfunding Platforms Africans Can Use For Business, Education, & More

Challenges and Recent Developments

1. Regulatory challenges

Over 18+ years, M-PESA has encountered significant regulatory hurdles.

In Kenya, authorities raised concerns about money laundering and consumer protection, prompting the introduction of know-your-customer (KYC) rules and transaction caps.

In 2018, the government imposed a 1.5% excise tax (later reduced) on mobile money transactions to boost revenue. Safaricom argued the tax disproportionately hurt the poor, leading Parliament to exempt small transactions.

Additionally, interoperability mandates were enacted to allow competing mobile money platforms to connect. However, Safaricom’s early lead meant it still benefited from network effects.

In global markets like India, regulators require banks to own mobile money ventures. As rules tightened in 2019, Vodafone was forced to wind down M-PESA operations in India.

2. Security and fraud concerns

M-PESA users have also faced security issues. In its early years, weak authentication protocols enabled fraudsters to trick users into revealing PINs or allowed agents to misappropriate funds.

SIM-swapping became a common threat, where attackers hijacked users’ phone numbers to drain M-PESA balances. To combat this, Safaricom invested heavily in fraud detection systems, frequent PIN updates, and extensive agent training.

Despite this, the shift from cash to mobile money introduced cybersecurity risks and privacy concerns.

For instance, manual agent-based KYC (copying IDs in notebooks) exposed users to identity theft, as noted by researchers at Carnegie Endowment. Safaricom has since adopted more secure digital KYC methods.

3. Product innovation in response to challenges

In response to regulatory and security issues, M-PESA has expanded its product offerings. It launched:

- M-Shwari (2013): A mobile savings and loan platform.

- Fuliza (2019): An overdraft service that allows users to complete transactions when their wallets are empty.

- Lipa na M-PESA (2013): Now a staple for merchant payments, driving cashless commerce in Kenya.

To improve access, Safaricom introduced USSD codes for basic phones and smartphone apps for seamless digital interaction.

It also ventured into international remittances—in 2012, Vodafone partnered with HomeSend to allow migrants to send money directly to M-PESA wallets across borders.

During COVID-19, M-PESA facilitated donations to relief funds and introduced loyalty rewards like cashback on Lipa na M-PESA purchases.

4. Regional expansion and continued innovation

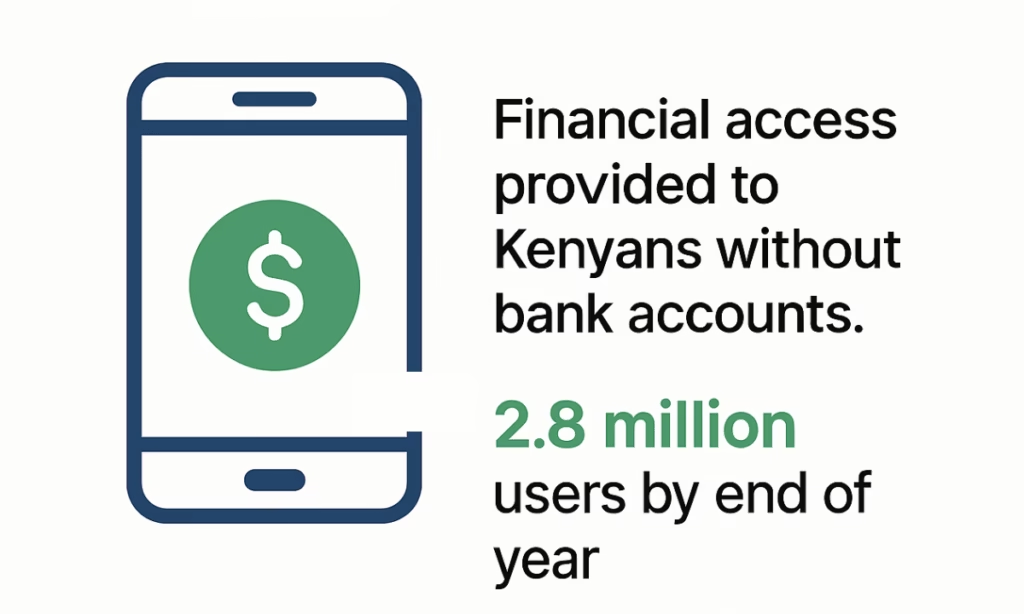

From 2021–2024, Safaricom expanded beyond Kenya by securing a telecom license in Ethiopia. By early 2025, M-PESA had:

- Gained 2.8 million customers

- Processed over KSh20.6 billion (~$156 million) in transactions within its first year

To boost user adoption in new markets and meet regulatory requirements, Safaricom partnered with Absa Bank to launch a deposit interest feature. Ongoing innovation includes:

- Overdrafts via Fuliza

- Credit scoring using airtime purchase behavior

- Data-driven lending tools

M-PESA remains an evolving platform, continuing to address its challenges with technology, policy dialogue, and regional growth strategies.

Why M-Pesa Succeeded & Lessons Learned

1. Solving a real problem with a user-centered approach

The M-PESA story began with a focus on a genuine need: Kenyans required a safe, low-cost way to send and receive money. While the original concept involved microloans, the team quickly pivoted to money transfers after observing user behavior.

As one insider noted, they “fell in love with the problem” – remittances – rather than any specific technology. This pivot, informed by user testing and on-the-ground feedback, laid the foundation for a truly customer-centric product.

Regular fee adjustments and field insights, particularly from rural users, helped shape a solution that met real-world needs.

2. First-mover advantage and market timing

M-PESA’s early entry into the mobile money space gave it a significant edge. Safaricom launched the service before any other player could compete at scale. This allowed them to capture public mindshare and build trust, setting a high bar for any future competitors. The timing also aligned with increased mobile phone penetration, amplifying its reach.

3. Agent network

A key element of M-PESA’s growth was its robust distribution network. Safaricom recruited local shopkeepers to serve as agents, leveraging Kenya’s existing informal retail structure.

This helped overcome the classic “chicken-and-egg” dilemma: agents attract users, and users attract agents. Safaricom smartly supported agents financially, providing initial float and commissions even before transaction volumes took off.

4. Regulatory collaboration, not confrontation

Rather than challenge financial authorities, Safaricom worked hand-in-hand with the Central Bank of Kenya. They agreed to formally register users and presented M-PESA as a complement to traditional banks rather than a rival. This collaborative, low-friction approach earned M-PESA legitimacy and trust from both regulators and the public.

5. Strategic partnerships expanded utility

M-PESA’s influence grew through strategic alliances. Partnering with banks enabled products like M-Shwari (mobile banking and savings), while deals with merchants supported bill payments and business services. These collaborations transformed M-PESA from a simple money transfer tool into a comprehensive financial ecosystem.

6. Leveraging Safaricom’s telecom infrastructure

Safaricom’s existing assets played a pivotal role: wide mobile network coverage, a massive subscriber base, and strong brand recognition. These elements gave M-PESA a built-in launchpad. Safaricom reinvested revenues to boost system reliability and expand the agent network, including subsidizing agent float and supporting mobile outreach.

7. Low fees, high volume

A critical decision was keeping transaction fees low. Though this meant lower revenue per transaction in the short term, it spurred wide usage. Safaricom understood that long-term value would come through increased customer loyalty, mobile data usage, and ecosystem entrenchment rather than immediate profit.

Lessons from M-PESA’s Playbook

M-PESA succeeded through a blend of innovation, adaptability, and alignment across stakeholders. Key takeaways include:

- Design for the user: Understand real pain points and iterate based on feedback.

- Solve a real problem – long travel and wait times for rural money transfers.

- Leverage existing infrastructure: Telecom networks and informal retailers were crucial.

- Build trust with regulators: Don’t disrupt blindly; engage and align with policy.

- Form strategic alliances: Banks, merchants, and fintech partners can expand your impact.

- Keep pricing inclusive: Affordability unlocks scale.

- Stay adaptable: Evolve your product, pricing, and partnerships as the market shifts.

- Be inclusive – low KYC barriers enabled mass adoption.

- Scale through partnerships – with banks (CBA, KCB), NGOs, government, and tech firms.

As Vodafone’s Nick Read put it, mobile money “benefits communities and helps create a multitude of small and micro-business ventures.” M-PESA’s journey is a masterclass for fintech entrepreneurs and policymakers alike.

Read Also: How to Pitch to Investors: A Guide for First-time African Founders

M-Pesa in Today’s Fintech Industry & Looming Challenges

1. M-PESA’s global recognition and blueprint status

M-PESA is widely recognized as Africa’s most influential fintech innovation, and one of the earliest and most successful examples of mobile money globally. By 2020, M-PESA had surpassed 40 million active users, mainly in Kenya, Tanzania, Ghana, Egypt, and Mozambique.

Its success inspired more than 140 similar platforms in 65 countries, including:

- India’s Paytm, which began as a mobile recharge and evolved into a full-fledged digital wallet. Though India has a far higher smartphone penetration, the core idea of easy mobile payments was seeded by M-PESA.

- Romania, where Vodafone launched an M-PESA pilot in 2014, but later shut it down due to low traction.

- Afghanistan, where M-PESA was piloted in partnership with Roshan Telecom as M-PAISA, particularly used for salary disbursement for policemen to curb corruption.

Despite varying degrees of success outside Africa, M-PESA remains the gold standard for mobile money in low-resource, high-need environments, especially where traditional banking infrastructure is weak.

In Kenya, it became so deeply entrenched that global giants like PayPal, Xoom, and Western Union had to integrate with it to access the Kenyan market, often finding themselves unable to compete on pricing or reach.

2. Driving and benefiting from the digital finance evolution

M-PESA didn’t just ride the digital finance wave — it helped shape it.

- M-Shwari, launched with Commercial Bank of Africa (CBA) in 2012, was one of the world’s first mobile-based savings and loan services. By 2018, M-Shwari had over 21 million users and had disbursed billions in microloans.

- M-PESA has since added:

- KCB M-PESA: A collaboration with Kenya Commercial Bank.

- M-TIBA: A health wallet used to pay for medical expenses.

- Insurance services: including crop insurance for farmers.

This ecosystem approach mirrors modern super app models, seen in Asia with WeChat Pay, Alipay, and Grab, but tailored to African needs and telecom infrastructure.

As smartphone adoption increases, M-PESA is gradually pivoting toward supporting apps, QR codes, and digital identity-linked services.

3. Expansion into new markets

Ethiopia, with a population of over 120 million and previously one of the largest untapped markets in Africa, opened its telecom sector in 2021. In 2022, Safaricom Ethiopia launched, and by 2023, M-PESA received approval to operate.

This expansion reflects M-PESA’s long-term ambition to be a pan-African fintech leader. Safaricom has framed Ethiopia as its “biggest growth frontier,” with M-PESA playing a central role in financial inclusion there.

In Safaricom’s FY2025 report:

- M-PESA generated US$1.25 billion in service revenue, accounting for 44% of total service revenue in Kenya.

- This proves M-PESA is not a legacy product, but a cash-generating growth engine.

Other markets under evaluation include DR Congo, Rwanda, and Nigeria, where mobile money regulations have recently opened up.

4. Legacy on the global stage: branchless banking pioneer

Before M-PESA, the prevailing view was that poor people needed physical banks to access financial services. M-PESA flipped that assumption:

- It created a branchless banking system using SIM card technology, USSD, and agent networks.

- The GSMA and CGAP (Consultative Group to Assist the Poor) have cited M-PESA in over 50 peer-reviewed publications as a case study for financial inclusion.

Its success inspired:

- bKash in Bangladesh: Backed by BRAC and later Ant Group, now one of the largest mobile money platforms globally.

- Opay in Nigeria: While built later in a more smartphone-first market, Opay’s model was also inspired by the agent-driven model popularized by M-PESA.

Its story is now taught at Harvard Business School, Oxford’s Said Business School, and Strathmore University as a foundational case in inclusive fintech innovation.

4. From classrooms to fintech playbooks

Academia and development organizations have studied M-PESA extensively:

- MIT, UC Berkeley, and LSE have all published research on its social and economic impact, particularly:

- Reducing poverty and financial shocks.

- Increasing women’s economic empowerment.

- Boosting rural access to credit.

Examples of academic papers:

- “The Long-run Poverty and Gender Impacts of Mobile Money” – Tavneet Suri & William Jack (Science, 2016)

- “Mobile Money and Risk Sharing Against Aggregate Shocks” – MIT working paper (2017)

Looming Challenges in a shifting fintech industry

Despite its success, M-PESA faces growing challenges:

- Smartphone penetration in Kenya is now over 50%, pushing users toward app-based wallets (e.g., Airtel Money, Chipper Cash, Flutterwave’s Send App).

- CBDCs (Central Bank Digital Currencies) are being explored across Africa, with Nigeria piloting the eNaira.

- Visa, Mastercard, and Stripe are aggressively expanding in Africa, targeting online merchants that M-PESA traditionally underserves.

- Diaspora remittances remain competitive:

- M-PESA has opened corridors with the UK, UAE, and Germany, but must compete on fees with apps like WorldRemit, Remitly, and Wise.

To stay ahead, M-PESA is:

- Building open APIs for merchants and startups.

- Partnering with PayPal, AliExpress, and others.

- Launching QR-code-based merchant payments (e.g., via Lipa na M-PESA).

- Exploring blockchain pilots and biometric KYC for enhanced security and compliance.

M-PESA as the backbone of Kenya’s digital economy

In Kenya today:

- Over 90% of households use M-PESA or similar mobile money services.

- It is integrated into public transport, utility bill payments, taxation (KRA eCitizen portal), and school fee payments.

- Small and micro enterprises rely on Lipa na M-PESA as their primary point-of-sale system.

Safaricom has rebranded itself as a tech platform, offering cloud, data, IoT, and financial services — all anchored by M-PESA.

Analysts argue that Kenya’s GDP is partly digitalized through M-PESA, making it arguably the most embedded fintech platform in a national economy globally.

See Also: Why Freelancing in Africa is Booming (& How You Can Profit From It)

Conclusion

M-Pesa’s story is more than a tale of financial innovation; it is a testament to how technology can leapfrog infrastructure gaps and empower entire populations.

From its modest beginnings as a microfinance experiment to becoming the financial lifeline of over two-thirds of Kenya’s population, M-Pesa has demonstrated how mobile technology can democratize access to financial services in even the most challenging environments.

Its success underscores the importance of user-centered design, robust partnerships, and relentless adaptation to local contexts.

As the fintech industry evolves in an increasingly digital and globalized economy, M-Pesa’s journey offers invaluable lessons on scalability, resilience, and inclusive growth.

While challenges such as regulatory shifts, competition, and technological disruption persist, M-Pesa remains a cornerstone of Africa’s digital economy and a beacon of what is possible when innovation meets real-world needs.

References drawn from these independent sources:

- Academic studies and industry reports on M-PESA’s launch, growth, and impact;

- Vodafone/Safaricom press releases and financial statements; and research by GSMA, World Bank, MIT, IPA, and others

Leave a comment and follow us on social media for more tips:

- Facebook: Today Africa

- Instagram: Today Africa

- Twitter: Today Africa

- LinkedIn: Today Africa

- YouTube: Today Africa Studio