In recent years, we have witnessed failed startups that have shut down in Africa and went under with over $200 million investor funds.

While the companies caved in under different circumstances, their exit is already raising concerns over the fate of many young innovative companies that are nursing the ambition of raising funds in the coming years.

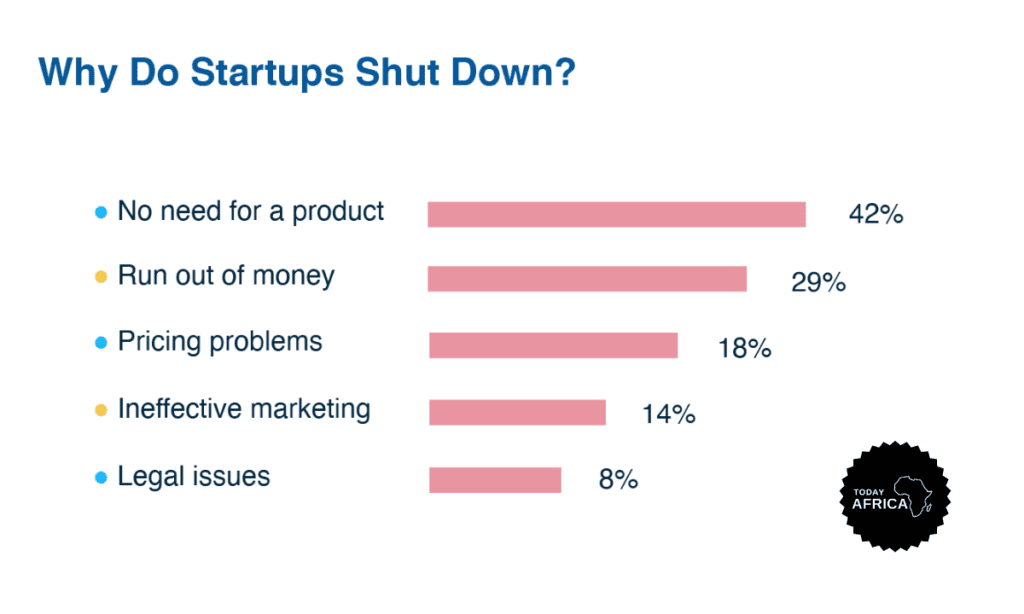

For one, venture capitalists have agreed that enough due diligence was not carried out in the past before funds were committed to most of the startups that have now failed.

This presupposes that any startup that will raise funds in the coming year would have to work harder and tick many boxes on the investors’ table before a cheque could be signed.

From 54Gene, which had raised $45 million to Pivo Africa, which packed up after raising $2.6 million from investors, the startups went under with millions of investors’ funds that may never be recovered.

17 Failed Startups in Africa

Pivo

- Launched: 2021

- Sector: Fintech

- Primary market: Nigeria

- Founders: Nkiru Amadi-Emina (CEO) and Ijeoma Akwiwu (COO)

- Total funding raised: $2.8 million

- Shutdown: December 2023

Pivo was a Nigerian digital bank aiming to serve the trade sector in Africa. In December 2023, the startup closed shop due to unresolved founder conflict, according to sources familiar with the matter. The reported conflict between Amadi-Emina and Akwiwu allegedly eroded Pivo’s reputation, damaged business relationships, fractured company culture, and disrupted team dynamics. These consequences significantly hampered the startup’s ability to secure future funding.

The shutdown happened a year after Pivo announced a $2 million seed round. Nkiru and Ijeoma bootstrapped Pivo for about six months before it became venture funding. Aside from YC, the Nigerian fintech was backed by Precursor Ventures, Vested World, FoundersX and Mercy Corp Ventures.

54gene

- Launched: 2019

- Sector: Biotech

- Primary market: Nigeria

- Founders: Abasi Ene-Obong

- Total funding raised: $94.7 million

- Shutdown: September 2023

Last year, Nigerian genomics startup 54gene faced a storm of controversy, including lawsuits, fraud allegations and valuation cuts, ultimately leading to the company’s shutdown.

Before its closure, 54gene faced internal turmoil. Co-founder and CEO Abasi Ene-Obong resigned, and his successor, Teresia Bost, the general counsel, later filed a lawsuit against the company alleging discriminatory behaviour and a hostile work environment. She named Ron Chiarello, her successor as CEO, as one of the defendants. Chiarello also left the company earlier this year.

“The company could not continue to operate financially, and it began to wind down in July,” Chiarello said. 54gene was previously named as one of Y Combinator’s 2023 top companies.

Passerine Aircraft

- Launched: 2017

- Sector: Aviation

- Primary market: South Africa

- Founders: Matthew Whalley

- Total funding raised: $120,000

- Shutdown: March 2020

Driven by the vision of runway-free takeoff, Whalley founded Passerine Aircraft, developing electric-powered delivery drones that utilised a novel jumping mechanism to achieve flight.

While the specific reasons for Passerine Aircraft’s closure haven’t been made public, the hardware-intensive nature of its electric drones likely contributed. As a capital-intensive industry, hardware development often requires significant funding beyond the initial $120,000 Y Combinator investment, which might have posed challenges for the startup.

Tress

- Launched: 2014

- Sector: Social commerce

- Primary market: Ghana

- Founders: Priscilla Hazel, Esther Olatunde, and Cassandra Sarfo

- Total funding raised: $120,000

- Shutdown: May 2018

Years ago, three female tech entreprenuers met at Meltwater Entrepreneurial School of Technology and collaborated to develop a social community app.

Tress aimed to empower women in their hairstyling journey. The platform served as a discovery tool, showcasing trendy styles with details on used products, stylists’ information, and pricing. Users could also share their personal favourites, exchange tips and techniques, and find support within a positive community.

Tress, a Ghanaian startup aiming to capture a share of the then $500 billion global haircare market, secured a spot in Y Combinator’s 2017 accelerator programme.

Despite generating significant online buzz, Tress ceased online activity in May 2018; The website and mobile app were not available. The co-founders also transitioned to other roles at that time.

Saida

- Launched: 2015

- Sector: Fintech

- Primary market: Kenya

- Founders: Kyale Mwendwa and Kenneth Ngetha

- Total funding raised: $120,000

- Shutdown: January 2022

When it launched in 2015, Saida, a Kenyan fintech startup, aimed to empower users by enabling them to manage their finances through separation, spending and tracking, as well as access to short-term loans based on mobile phone activity data.

Read Also: 15 Startup Success Stories: From Ideas to Millions

While the specific reasons behind Saida’s shutdown remain unclear, co-founder Ngetha has since transitioned to venture-building engagement at Catalyst Fund.

Other African Failed Startups

Across Africa, the number of startups that are shutting down has continued to rise. In August, Kenyan end-to-end fulfillment startup Sendy shut down operations and announced an assets sale with reports saying reduced order volumes and fuel price hikes meant it was making deliveries at a loss, and had a monthly burn rate of US$1 million.

Sendy raised US$20 million in capital as recently as January 2020, but in the current climate, further funding was not to be found.

Ghanaian payments startup Dash, founded in 2019, had raised a whopping US$86 million, but folded in October amid allegations of financial impropriety and false reporting.

South African mobility startup WhereIsMyTransport, bankrolled to the tune of over US$27 million by investors such as Naspers in recent years, announced it was closing down in October after failing to secure more investment.

Kenyan B2B e-commerce startup Zumi had earlier in March announced it had closed down after failing to secure the necessary funding to continue operations. Launched in 2016, Zumi began life as a female-focused digital magazine, before pivoting into e-commerce in 2020.

According to co-founder and CEO William McCarren, the startup achieved over US$20 million in sales, acquired 5,000 customers and built a team of 150 people, but closed after failing to secure investment.

Another Kenyan e-commerce company Copia, which raised US$50 million Series C funding last year, announced it was pulling out of Uganda, “consistent with many of the best companies in Africa and across the world which are responding to the market environment and prioritising profit.”

Failed Startups in Nigeria

Lazerpay

After making the headlines as a company founded by 19-year-old Njoku Emmanuel and went on to raise $1.1 million, Lazerpay, a web3 crypto payments company, on April 13, 2023, announced it was shutting down, to everyone’s surprise. This came a few months after the startup had laid off some of its staff to extend its runway as it sought investors.

However, the expected additional investment did not come.

“Today, we announce the difficult decision to cease operations at Lazerpay. Despite our team’s tireless efforts to secure the necessary funding to keep Lazerpay going, we were unable to close a successful fundraising round. We fought hard to keep the lights on as long as possible, but unfortunately, we are now at a point where we need to shut down,” Njoku said as the company wound down.

Bundle Africa

Nigerian crypto startup Bundle Africa announced that it would shut down its social payments app Bundle Africa. In a tweet announcing the shutdown, CEO Emmanuel Babalola said that the shutdown was a decision made by stakeholders who want a restructuring of the company.

This came after the company had raised $450,000 in a pre-seed that had participation from two investors.

However, unlike others, investors in Bundle Africa may not have lost it all as the startup now focuses on Cashlink, its peer-to-peer platform. The company reportedly hit 50,000 monthly active users and a $50 million monthly volume on Bundle and crossed over 3 million transactions on Cashlink.

Payday

Similarly, fintech company, Payday, ran into a problem barely 6 months after raising $3 million in a seed round led by Moniepoint. The company’s founder and CEO, Favour Ori, was alleged to be paying himself a monthly salary of $15,000 at the expense of the company’s survival while employees were made to take pay cuts. The company had also faced serious allegations of fraud from customers as their accounts were restricted without any explanation until they cried out on social media.

Early this month, it was announced that Payday has been acquired by Blockchain payments platform, Bitmama Inc.

Zazuu

Zazuu, a fintech company founded in 2018 by four Nigerian entrepreneurs, Kay Akinwunmi (CEO), Korede Fanilola (COO), Tosin Ekolie (CTO) and Tola Alade (CDO), shocked the tech and finance industry when it announced on November 17, 2023, that it was shutting down operations.

The firm’s management attributed the shutdown to its inability to secure additional growth funding from investors.

The company, an end-to-end money transfer marketplace that facilitated remittance payments into Sub-Saharan Africa, had in July 2023, raised $2 million to deepen its cross-border payment offering and also build the world’s first non-biased payment platform.

Angel investors that participated in the fundraising round are Babs Ogundeyi, chief executive officer of Kuda Bank and Jason Njoku, chief executive officer of IrokoTV. Other angel investors include Launch Africa, Founders Factory Africa, HoaQ Club and Tinie Tempah.

While raising the funds last year, the startup assured that it would continue to grow its user base, hire more talent, and scale its pay with the Zazuu feature that allows users to complete transactions in-app.

Vibra

Exactly two years ago in December 2021, Nigeria-based African Blockchain Lab, Vibra raised $6 million in a pre-Series A round co-led by a consortium of global investors, including renowned African venture capital firms Lateral Frontiers VC, CRE Venture Capital and Musha Ventures, as well as international blockchain investors Dragonfly Capital, Hashkey Capital, SNZ Capital, Fenbushi, Cadenza Capital, Head & Shoulder X, LeadBlock, Hash Global, Bonfire, Krypital, Despace and more.

The funding was to see Africa Blockchain Lab roll add new features like VIBRA Earn, a crypto asset saving product that lets users earn interest on a variety of crypto assets. However, in July this year, the company shut down its operations, not only in Nigeria but also in Kenya and Ghana.

Okadabooks

Founded in 2013 and a pioneer in digital publishing and bookselling, Okada Books, closed down in November this year after 10 years of operation, citing rough macroeconomic conditions.

“We explored various avenues to keep our virtual bookshelves alive but, unfortunately, the challenges we face are insurmountable,” said Okechukwu Ofili, the company’s CEO, in a social media statement.

In 2017, Okadabooks was among 12 startups selected for Google’s Launchpad Accelerator Africa.

Hytch

In February, Nigerian logistics startup Hytch confirmed it had shut down barely nine months after launch.

“It has been a tough one but we are shutting down operations finally,” the company said in a social media post. We would no longer be providing our services to businesses or individuals,” the company said in a statement.

The closure came about after it failed to secure further funding.

Time For Due Diligence

Disturbed by the rate of failed startups witnessed in Nigeria this year, venture capitalists are blaming the development on the poor decisions made by investors in the last two years.

A good due diligence process shoots to understand your business and you as a founder. Good investors aim to balance that with optimizing for materiality, reasonableness, and, yes, pace.

The process is also your chance to get to know the character and expertise of the investor. Nobody is helped — not you or the investor — by optimizing for speed.

Times are tougher, yes, but if nothing else, this fundraising winter is also a good chance to reset and rediscover a healthier, more sustainable long-term dynamic between founders and investors in Africa tech & VC.